I hate loving General Electric (GE), its like an ex boyfriend/girlfriend that broke your heart.

Each time you go back, you tell yourself it will be different... they have changed! Yet every time you go back, they break your heart again.

This has now happened to me twice with GE. In 2008, I was riding high, having bought GE in the mid 20"s in 2004, with the promise of an industrial revolution. The finance division was booming and I was up a cool 50% and thought I had found the one!

Then I found out they were cheating on me with someone named subprime! It nearly bankrupted the company, and Uncle Warren had to come to the rescue to save it.

I was frankly, lucky to get out when I did, selling mid panic in the low 20"s. The end result was a 4 year investment that returned roughly negative 20%. I vowed to never make that mistake again...

In early 2015, it was as if GE sent me a text saying... "I miss you... lets get lunch to catch up?" and unfortunately for me, I hit reply. And just like that, we were back together.

The stock had been consolidating all year, and Jeff Immelt had on his shiniest used car salesmen hat, singing sweet nothings into my ear of buybacks, the disposal of the finance assets and refocusing on core industrial operations.

Blah, blah, blah! Next thing I know, this pretty little stock I re bought at 24 and had me sitting on 35% gains, gets cut in half... Apparently the company had a nasty secret spending habit they hid for years and years.

GE data by YCharts

GE data by YChartsSo I had a decision to make mid 2017, do I bail again and take another 20%+ loss? Is this stock destined to break my heart again and again until nothing is left?

I did some soul searching... deep in the woods. And had decided again to leave, never to return.

But as I was leaving the door, with my bags packed, and my prized, signed picture of the Jamaican bobsled team in toe, an event made me hit the pause button.

Jeff Immelt had decided to "step down."

This left me in a holding pattern for months, until Nov 13th. When new CEO John Flannery issued 2018 guidance that was, lets be kind and just say disastrous. Lowering even the lowest of bars for 2018 to EPS of $ 1-$ 1.07.

So, why am I still a holder of GE stock?

To squeeze some more juice out of my "ex" metaphor, GE just checked itself into rehab!

It now realizes it has a serious problem, it has overspent and or had disastrous timing on virtually every major deal it has done in the last 10-15 years. Alstrom, check. Oil assets, check. Finance disposal, check. Buyback, check.

Mr Flannery appears to not need a second corporate jet to follow him around "just in case" unlike Mr Immelt. He also seems to be dead set on costs, which with GE in its current structure will keep him busy for a while.

Why not close your position?

You think I am crazy don"t you, why in the world would I consider keeping or perhaps doubling my position in a stock that has done nothing but hurt me?

The reason is pretty simple, all of the dirty laundry appears to be in the open now. No more secret spending accounts or ill researched / timed acquisitions (for now). Mr Flannery has all but told anyone that will listen that the rest of 2017 and all of 2018 will suck, and to not invest.

He didn"t "kitchen sink" an earnings report, he lit the whole house on fire.

Source: Meme Generator | Create Your Own Meme

Mr Flannery has called for a new approach to doing business at GE and more importantly to transparency, apparently not subscribing to Immelt"s pyramid scheme like approach to GE"s cash flow. He has acknowledged the pension shortfall, which I am sure will come up in the comments section of this article. Also shrinking the board from a frat house of 18 to a GE focused 12, preaching honesty (imagine that) and accountability in the new GE.

So far I am digging the new CEO and currently am in tacit agreement with his broad outline.

What was the new CEO given to work with?

I"m glad you asked! GE in my opinion has a very strong set of business"s to work with, below I have outlined the 6 major divisions it currently operates.

Power- GE"s power business is huge, with an installed base in every major country in the world. They claim to produce 1/3rd of the worlds electricity through gas, steam and nuclear turbines. This is a core division for GE, and one that recently has helped drive them directly into a ditch, as overcapacity, technical issues and in my view an ill timed Alstrom acquisition weigh on earnings at the division.

However, GE power does have many redeeming qualities. They are a technology leader in the industry whilst having deep relationships with customers in a field that honestly does not have all that many options. Near term however, look for deep cuts in expectations at the unit until the smoke clears.

Aviation- The companies Aviation segment has been a bright spot in recent results, with continued wins and new product introductions, for example LEAP, its new narrow body engine that from what I can find is truly state of the art, with a 15% fuel improvement, increased reliability, weighs 500 lbs less and is 3D printed (which, lets face it, is just cool!)

This division looks set to continue to preform well in the near term and may be looked at as an example for the rest of the company.

Transportation- The transportation segment is mostly composed of GE"s rail assets and is thought to perhaps be on the chopping block for divestiture. They build locomotives with a large portion of revenue coming from the services side of the business, which is something I like to see. They are a global leader in the industry and the mix of technology and services is impressive.

However the division has been lackluster of late and the strategic fit is questionable and thus may not make sense for them to keep. They did just win a 200 locomotive order from Canadian National Railway (CNI) but it may be prudent to offload this asset to focus on core business.

I sort of hate to see this business go, as it truly is world class. However GE hopefully will use proceeds here to either reduce debt or shore up the oft cited pension shortfall.

Healthcare- GE has a broad and diverse set of healthcare assets, providing imaging, healthcare cloud, cardiology, orthopedics and anesthesia equipment, among multiple other products and services.

This has been a strong performer for the company and what I would consider another core holding of GE, this division looks to be a good fit with its digital offerings and will likely continue to buoy the company during this current slump.

BHGE- This is a division that really makes me mad, and I struggle to remain calm in my writing. Jeff Immelts timing was so bad that it feels like it was on purpose. Immelt decided to buy a bunch of oil services companies, seemingly at the absolute top of the oil market. Grrr.

Anyways, GE Baker Hughes as it is now called is the 2nd largest oil services company in the world and to be fair is actually a very good company, and is a technology leader in the industry along side Halliburton (HAL). So basically it is the second prettiest girl in a leper colony.

Oil services, seem in my opinion to be stuck in a pretty serious long term rut and GE, I believe will look to dispose of this asset likely through a spin off off or divestiture of its stake rather quickly. Perhaps GE could offer Immelt a stake in this spin off in return for the GE stock he so graciously awarded himself during his charade.

Renewables- The renewables division is home to a world class wind energy turbine manufacturer, along with in my opinion is the most valuable part, its services segment. GE has established itself as the worlds number 2 wind turbine company behind Vestas Wind Energy (OTCPK:VWDRY). The company also has an emerging offshore wind and hydro power segment that are lacking scale currently, but hold long term promise.

The wind market this year has suffered from intense competitive pressures thus dragging results, however this also looks to be a core division for GE in the future.

So why am I sticking with GE this time - and may be looking to "pop the question" soon?

The companies potential is just so damn pretty! GE lines up well with my vision of the mega trends of the future.

In my mind, a company must both show an ability for growth, while possessing a solid balance sheet with operating discipline from which to build. Under Mr Immelt, GE, in hindsight obviously stood much closer to the crazy side of Mr Barney Stinson"s famed graph below.

Source: FANDOM

Mr Flannery seems to be dead set on adjusting the results of the above graph.

After the dust settles from the recent house fire Mr Flannery has set ablaze, I am envisioning 4 major divisions of GE remaining. Power, Aviation, Healthcare & Renewables.

All 4 remaining divisions fit into my vision- with 3 qualifying in my mind as mega trends. Power, Aviation & Renewables.

Healthcare I view as a great business as well but does not fit as a mega trend in my book with so many unknowns as to the future in the industry.

Power- Power is (obviously) a key need for the future as more and more countries look to move to gas powered plants and away from coal. With the world estimated to need an additional 50% more electricity in the next 20 years, perhaps adding dramatically to that if the electric car revolution is indeed realized.

GE is in great shape position wise in the industry and once the fat has been cut, along with a renewed focus on execution, this division should prove to be a key driver of profits for decades to come.

The below graph shows an estimate of the worlds need for energy into 2035.

Source: Breaking Energy

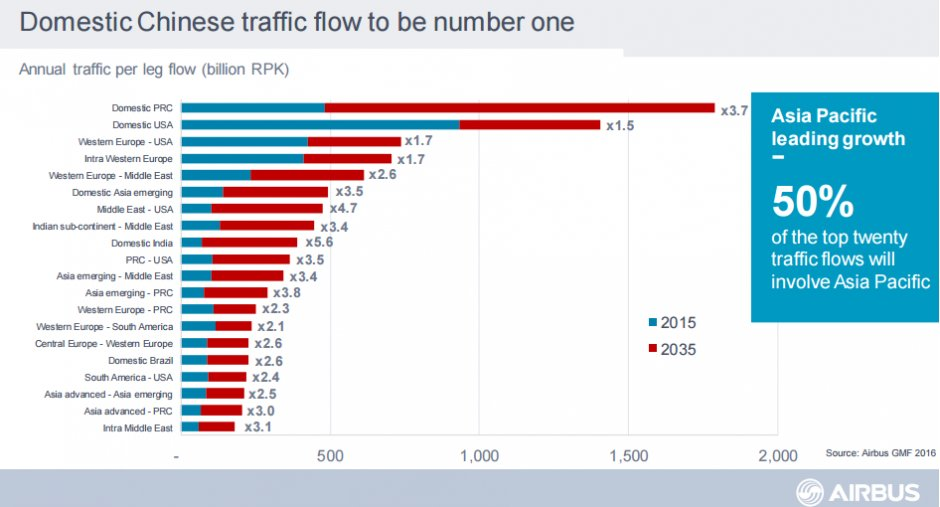

Aviation- This division looks to be in the midst of a multi decade run, as the world continues to be more interconnected. Importantly the Asian travel market is in the early innings of what looks to be a spectacular expansion. GE I believe is in the drivers seat in this industry, both in technology and services.

My one worry is the Chinese looking to enter this market with "homegrown technology" which I believe is code for stealing IP and re packaging it. However manufacturing jet engines is an entirely different animal from copying an iPhone and progress on a Chinese engine that is both safe and accepted is likely a few decades off.

Source: Airbus Home Healthcare- This industry as a whole, especially preventative medicine in my view will swell massively in the next few decades. I am going to lose a few followers over this i"m certain but I believe universal healthcare in the United States is pretty much a sure bet sometime in the next 20 years. Which would be good news for GE! Keeping costs down will likely be a key requirement of any future health system, and with GE"s expertise in imaging for preventative medicine and its emerging analytics and software offerings, it may be able to play an important role in the health systems future, however uncertainties do exist as to the nature of cost controls and the potential for margin compression in all things health related. Committee for a Responsible Federal Budget Renewables- I am firmly on the alternative energy bandwagon and GE"s positioning in this industry appears very ideal. Wind energy by most measures is already roughly equal in cost per MWh to current fossil fuel plants, this will likely get better with time, and with offshore wind and hydro picking up steam in both efficiency and scale for GE, will open further avenues of growth for this division. Alternative energy is here to stay, and GE looks to be on a path that requires no subsidies, a major pitfall to solar currently. The downside to wind energy could be the commoditization of wind turbines, however I believe that GE has the technology and service capability to differentiate themselves in this rapidly growing industry for decades to come. Source: U.S. Energy Information Administration (NYSEMKT:EIA) GE has burned me... Badly in the past, and I must say I am rather gun shy about committing to a perhaps multi decade long marriage to the stock. But she is so damn pretty! Source: Meme Generator | Create Your Own Meme My plan "as of today" is to keep my current position, roughly 2.2% of my equity portfolio in GE for the first half of 2018, to test the waters, if you will, of the new CEO. If I continue to like what I am seeing and the valuation seems fair, which I view it to be currently (a forward PE of 17ish) I may step up to the plate and double my position in the company. Or maybe I won"t, and I will just run like heck and never come back! GE: "Hey you, what"s up" Me: ... Author"s note: If you enjoyed this article and would like to be notified of my future articles, please hit "follow" next to my name at the top of the article to receive notification of future articles I publish. Disclosure: I am/we are long VWDRY, GE. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Editor"s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

So will I say "I do"?

Tech

No comments:

Post a Comment