Free web hosting can be very enticing to individuals and businesses that do not have enough money to afford good web hosting services. But is it something worth the time spent and efforts done?

Fortunately there are proven ways on how to determine the most suited web host for your requirements. First you have to do an extensive research. Gather as many information on free web hosting services. You can always do this by doing an online search at google or yahoo.

After compiling your list then decide the service that you want from a web host. Consider the advantages and disadvantages of availing the services of a particular web host. You might also want to ask around. Actually there are a lot of discussion forums on the Internet regarding free website hosting. Go around discussion boards and read. You can also ask people who have availed of free website hosting about their experiences in getting a free hosting service. This is a good way for you to learn about the pros as well as cons of getting such service.

Free web hosting also gave its users with sub domain name, making it almost impossible to be searched on in various search engines. This made most websites on free web host servers almost impossible to be found on search engines. Reliability was also a concern, troubling most business owners who availed of free website hosting. With all these problems arising, there"s little doubt that getting free website hosting is not that practical. It will not help websites particularly those selling products and services.

Remember, every free hosting firm will try to make money from your website. Look for a hosting firm, which is less intrusive and more reliable.

About the Author:

Learn more about dedicated hosting web and get a Free limited report on Web Hosting Insights, a popular website that provides free tips and advice on web hosting solutions.

TORONTO (Reuters) - Facebook Inc plans to open an artificial-intelligence laboratory in Montreal, which will be run by prominent AI researcher Joelle Pineau, two people familiar with the plan said on Friday. Tech

Free web hosting can be very enticing to individuals and businesses that do not have enough money to afford good web hosting services. But is it something worth the time spent and efforts done?

Fortunately there are proven ways on how to determine the most suited web host for your requirements. First you have to do an extensive research. Gather as many information on free web hosting services. You can always do this by doing an online search at google or yahoo.

After compiling your list then decide the service that you want from a web host. Consider the advantages and disadvantages of availing the services of a particular web host. You might also want to ask around. Actually there are a lot of discussion forums on the Internet regarding free website hosting. Go around discussion boards and read. You can also ask people who have availed of free website hosting about their experiences in getting a free hosting service. This is a good way for you to learn about the pros as well as cons of getting such service.

Free web hosting also gave its users with sub domain name, making it almost impossible to be searched on in various search engines. This made most websites on free web host servers almost impossible to be found on search engines. Reliability was also a concern, troubling most business owners who availed of free website hosting. With all these problems arising, there"s little doubt that getting free website hosting is not that practical. It will not help websites particularly those selling products and services.

Remember, every free hosting firm will try to make money from your website. Look for a hosting firm, which is less intrusive and more reliable.

About the Author:

Learn more about dedicated hosting web and get a Free limited report on Web Hosting Insights, a popular website that provides free tips and advice on web hosting solutions.

Privacy, Facebook, surveillance, net neutrality, gender issues, climate change, hacking: The list of opinion topics that most attracted attention from WIRED readers in 2017 doubles as a list of Things That Gave Us Angst This Year. Here are the dozen most-read Opinion pieces of 2017.

The Federal Communications Commission’s vote to kill net neutrality provisions drew derision from all corners of WIRED, including our opinion section, which ran severalop-eds on the topic. In December Ryan Singel, a former WIRED editor who’s now a media and strategy fellow at the Center for Internet and Society, argued that ending the open internet will have profound effects on the re-election efforts of Congressional Republicans in 2018.

In August, shortly after Google engineer James Damore posted a diatribe about gender differences on an internal company message board, UC San Diego physics professor Alison Coil explained why male scientists devalue research that identifies gender bias in the field. Academics should believe the research showing discrimination, but, Coil asserted, "What this extensive literature shows is, in fact, scientists are people, subject to the same cultural norms and beliefs as the rest of society."

Last January, as California was saturated with rain and snow, the Pacific Institute’s Peter Gleick, a hydroclimatologist, explained why a wet year didn’t mean the golden state’s drought was over. Nearly a year later, as the state has been incinerated by historically terrible wildfires, it’s all too clear that Gleick was right.

What should government do when a company fails to protect the personal data of 143 million people? Give it the corporate version of the death penalty, argued Ron Fein, the legal director of Free Speech for People. Fein"s October essay explained that in Georgia—Equifax’s home state—authorities can file suit to dissolve a corporation if it has abused the authority conveyed upon it by the state.

Hossein Derakhshan, an Iranian-Canadian media analyst, wrote that the rise of social media is reducing humans’ curiosity, as people strive for Likes rather than the pursuit of knowledge. Social media, Derakhshan argued, “engages us in an endless zest for instant approval from an audience, for which we are constantly but unconsciously performing.”

In February Benjamin Sanderson, a climate scientist at the National Center for Atmospheric Research, warned that a top candidate to be Donald Trump’s science advisor, William Happer, was a climate change enthusiast. Ultimately, Happer didn’t get the job, but the position is still vacant.

Not every question can be answered with code, Emma Pierson, a physics PhD candidate at Stanford, wrote in April. When ethical questions arise in, say, artificial intelligence applications, sound knowledge of other fields—literature, sociology, or ethics, for example—will help uncover solutions that algorithms alone cannot.

February’s match-up between the New England Patriots and Atlanta Falcons ended with a killer comeback for the Patriots. Jeff Ma, the leader of the MIT blackjack team that inspired the book Bringing Down the House, explained that the Falcons lost because the team didn’t follow basic probability rules commonly employed at a blackjack table.

Given the tremendous amount of attention given to Donald Trump’s tax returns, it’s almost inconceivable that they haven’t already been hacked, wrote John Powers, who runs a New York-based investigative firm, in November.

In November Antonio García Martínez, who was the first ads targeting product manager on Facebook’s ads team, wrote that Facebook isn’t eavesdropping on its users through their smartphones’ microphones. That’s in part because the social network tracks users so many other ways, it doesn’t need to snoop.

Writer and technologist Jason Tashea explained how algorithms pervade our everyday lives, from our credit scores to the route Waze suggests we take to the airport. Tashea argued that applying algorithms in criminal cases, with no clear oversight or transparency, could result in overly punitive sentences.

As WIRED editors have explained at length, devices like Amazon’s Echo and Google Home series listen to our conversations, eagerly awaiting a “wake” word to command them to turn on some Miriam Makeba or calculate how many tablespoons are in a cup (16). But, as civil attorney Gerald Sauer explained in a February piece, smart home devices’ microphones can also effectively collect evidence that can be used against their owners in court.

As we explained in Part 1, the most dangerous place on the planet financially is now the Wall Street casino. In the months ahead, it will become ground zero of the greatest monetary/fiscal collision in recorded history.

For the first time ever both the Fed and the US treasury will be dumping massive amounts of public debt on the bond market---upwards of $1.8 trillion between them in FY 2019 alone---and at a time which is exceedingly late in the business cycle. That double whammy of government debt supply will generate a thundering "yield shock" which, in turn, will pull the props out from under equity and other risk asset markets----all of which have "priced-in" ultra low debt costs as far as the eye can see.

The anomalous and implicitly lethal character of this prospective clash can not be stressed enough. Ordinarily, soaring fiscal deficits occur early in the cycle. That is, during the plunge unto recession, when revenue collections drop and outlays for unemployment benefits and other welfare benefits spike; and also during the first 15-30 months of recovery, when Keynesian economists and spendthrift politicians join hands to goose the recovery----not understanding that capitalist markets have their own regenerative powers once the excesses of bad credit, malinvestment and over-investment in inventory and labor which triggered the recession have been purged.

By contrast, the Federal deficit is now soaring at the tail end (month #102) of an aging business expansion. And the cause is not the exogenous effects of so-called automatic fiscal stabilizers associated with a macroeconomic downturn, but deliberate Washington policy decisions made by the Trumpian GOP.

During FY 2019, for example, these discretionary plunges into deficit finance include slashing revenue by $280 billion, while pumping up an already bloated baseline spending level of $4.375 trillion by another $200 billion for defense, disasters, border control, ObamaCare bailouts and domestic pork barrel of every shape and form.

These 11th hour fiscal maneuvers, in fact, are so asinine that the numbers have to be literally seen to be believed. To wit, an already weak-growth crippled revenue baseline will be cut to just $3.4 trillion, while the GOP spenders goose outlays toward the $4.6 trillion mark.

That"s right. Nine years into a business cycle expansion, the King of Debt and his unhinged GOP majority on Capitol Hill have already decided upon (an nearly implemented) the fiscal measures that will result in borrowing 26 cents on every dollar of FY 2019 spending. JM Keynes himself would be grinning with self-satisfaction.

Moreover, this foolhardy attempt to re-prime-the-pump nearly a decade after the Great Recession officially ended means that monetary policy is on its back foot like never before.

What we mean is that both Bernanke and Yellen were scared to death of the tidal waves of speculation that their money printing policies of QE and ZIRP had fostered in the financial markets. So once the heat of crisis had clearly passed and the market had recovered its pre-crisis highs in early 2013, they nevertheless deferred, dithered and procrastinated endlessly on normalization of interest rates and the Fed"s elephantine balance sheet.

So what we have now is a central bank desperately trying to recapture lost time via its "automatic pilot" commitment to systematic and sustained balance sheet shrinkage at fixed monthly dollar amounts. This unprecedented "quantitative tightening" or QT campaign has already commenced at $1o billion of bond sales per month (euphemistically described as "portfolio run-off" by the Eccles Building) during the current quarter and will escalate automatically until it reaches $50 billion per month ($600 billion annualized) next October .

Needless to say, that"s the very opposite of the "accommodative" Fed posture and substantial debt monetization which ordinarily accompanies an early-cycle ballooning of Uncle Sam"s borrowing requirements. And the present motivation of our Keynesian monetary central planners is even more at variance with the normal cycle.

To wit, they plan to stick with QT come hell or high water because they are in the monetary equivalent of a musket reloading mode. Failing to understand that the main street economy essentially recovered on its own after the 2008-2009 purge of the Greenspanian excesses (and that"s its capacity to rebound remains undiminished), the Fed is desperate to clear balance sheet headroom and regain interest rate cutting leverage so that it will have the wherewithal to "stimulate" the US economy out of the next recession.

Needless to say, this kind of paint-by-the-numbers Keynesianism is walking the whole system right into a perfect storm. When the GOP-Trumpian borrowing bomb hits the bond market next October we will already be in month #111 of the current expansion cycle and as the borrowing after-burners kick-in during the course of the year, FY 2019 will close out in month #123.

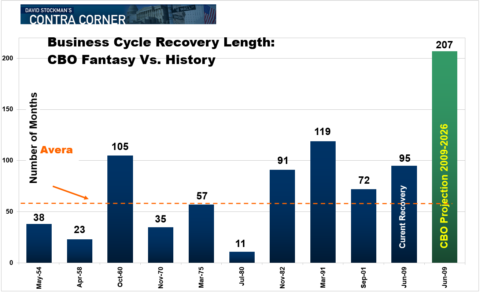

Here"s the thing. The US economy has never been there before. Never in the recorded history of the republic has a business expansion lasted 123 months. During the post-1950 period shown below, the average expansion has been only 61 months and the two longest ones have their own disabilities.

The 105 month expansion during the 1960s was fueled by LBJ"s misbegotten "guns and butter" policies and ended in the dismal stagflation of the 1970s. And the 119 month expansion of the 1990s reflected the Greenspan fostered household borrowing binge and tech bubbles that fed straight into the crises of 2008-2009.

Yet the Trumpian-GOP has not only presumed to pump-up the fiscal deficit to 6.2% of GDP just as the US economy enters the terra incognito range of the business cycle (FY 2019); it has actually declared its virtual abolition. Ironically, in fact, on December 31, 2025 nearly all of the individual income cuts expire----meaning that in FY 2026 huge tax increases will smack the household sector at a $200 billion run-rate!

But not to worry. The GOP"s present-day fiscal geniuses insist that the current business expansion, which will then be 207 months old, will end up no worse for the wear. The public debt will then total $33 trillion or 130% of GDP---even as the US economy gets monkey-hammered by huge tax increase.

Alas, no harm, no foul. The business expansion is presumed to crank forward through FY 2027 or month #219.

Needless to say, the whole thing degenerates into a sheer fiscal and economic fairy-tale when you examine the data and projections. But that hasn"t deterred the GOP"s fiscal dreamers.

Not only have they implicitly embraced an out-of-this-word 219 month business cycle expansion, but they have also insisted it will unfold at an average nominal GDP growth rate that has not been remotely evident at any time during the 21st century.

As shown in the chart below, the 10-year CBO forecast of nominal GDP (yellow line) is already quite optimistic relative to where GDP would print under the actual growth rate of the last ten-years (blue line). In fact, the CBO forecast generates $16 trillion of extra GDP and nearly $3 trillion more Federal revenue than would a replay of the last 10-years---and notwithstanding the massive fiscal and monetary stimulus during that period.

Still, the GOP/Trump forecast (grey line) assumes a full percentage point of higher GDP growth on top of CBO and no intervening recession and resulting GDP relapse.

Accordingly, the GOP assumes $30 trillion of extra GDP over the coming decade or nearly 23%more than would be generated by the actual growth rate (blue line) of the last decade; and consequently, $6 trillion of extra revenue.

That"s right. An already geriatric business cycle is going t0 rear-up on its hind legs and take off into a new phase of growth in the face of an epochal pivot of monetary policy to QT and a public debt burden relative to GDP that is approaching a Greek-style end game.

(Note: Figures in the box are inverted. First line should be 2006-2012 redux and third line should be Trump forecast.)

Stated differently, fiscal policy has descended into the hands of political mad-men at the very time that monetary policy is inexorably slouching toward normalization. Under those circumstances there is simply no way of avoiding the "yield shock" postulated above, and the cascading "reset" of financial asset prices that it will trigger across the length and breadth of the financial system.

As usual, however, the homegamers are the last to get the word. The unaccountable final spasm of the stock market in 2017 will undoubtedly come to be seen as the last call of the sheep to the slaughter. And owing to the speculative mania that has been fostered by the Fed and its fellow-traveling central banks, it now appears that the homegamers are all-in for the third time since 1987.

Indeed, Schwab"s retail clients have never, ever had lower cash allocations than at the present time---not even during the run-up to the dotcom bust or the great financial crisis.

But this time these predominately baby-boom investors are out of time and on the cusp of retirement---if not already living on one of the Donald"s golf resorts. When the crash comes they will have no opportunity to recover----nor will Washington have the wherewithal to stimulate another phony facsimile of the same.

The GOP-Trumpian gang has already blown their wad on fiscal policy and the Fed is stranded high and dry still close the zero-bound and still saddled with an elephantine balance sheet.

That is, what is fundamentally different about the greatest financial bubble yet is that there is no possibility of a quick policy-induced reflation after the coming crash. This time the cycle will be L-shaped----- with financial asset prices languishing on the post-crash bottom for years to come.

And that is a truly combustible condition. That is, 65% of the retirement population already lives essentially hand-to-month on social security, Medicare and other government welfare benefits (food stamps and SSI, principally). But after the third financial bubble of this century crashes, tens of millions more will be driven close to that condition as their 401Ks again evaporate.

That"s why the fiscal game being played by the Donald and his GOP confederates is so profoundly destructive. Now is the last time to address the entitlement monster, but they have decided to throw fiscal caution to the winds and borrow upwards of $1.6 trillion (with interest) to enable US corporations to fund a new round of stock buybacks, dividend increases and feckless, unproductive M&A deals.

Then again, what the GOP has not forgotten is the care and feeding of its donor class. That mission is being accomplished handsomely as it fills up the deep end of the Swamp with pointless, massive defense spending increases and satisfies K-Street with a grotesquely irresponsible tax bill that was surely of the lobbies, by the PACs and for the money.

At the end of the day, however, the laws of free markets and sound finance will out. The coming crash of the greatest bubble ever will prove that in spades.

The future, according to the folks who make the renderings, will be built mostly around whooshing. The details differ from one imagined utopia to the next, but the broad strokes are the same. Cars will run on electricity, drive themselves, even fly. Networks of vacuum tubes and tunnels will connect cities to each other and to the hinterlands. Supersonic jets will turn transoceanic journeys into river crossings. The burning of fossil fuels will seem as remote and unsavory as human sacrifice. Trees will blanket the urban centers; the air will refresh our lungs instead of blackening them.

Moving about the planet will be faster, safer, easier, comfier, greener, cheaper, and whooshier. Best of all, there will be no traffic.

So say the renderings, of which there are many. They’re created by all the players who imagine themselves profitably managing this future—Elon Musk chief among them, but also Lyft and Uber, Ford and General Motors, and innumerable startups.

Ford—which now calls itself a mobility company as well as an automaker—is among the many companies pitching a new, utopian vision of the future.

FOrd

Americans have been given a glimpse of this sort of transportation paradise before. They stood under the hot sun for hours at a time to see it, because they were fed up with traffic, and any world that promises to end it is worth a look. And so millions of people made it up a winding ramp and into a mysterious building and sat in the navy blue mohair chairs that would ferry them through the marquee exhibit of the 1939 New York World’s Fair.

The progenitor of the optimism-soaked hybrid of amusement park and educational diorama later perfected by Walt Disney, Futurama was a 17-minute pitch by General Motors that showed its audience a world that had solved transportation by signing over the ground floor of city and country to the car. Everyone in the picture had the keys to that era’s smartphone, the device that unlocked access to a world of wealth and convenience.

That vision, for the most part, came true. Futurama predicted the world of 1960. By that new decade, the personal car was in fact dominant, suburbs reigned supreme, and the highway was everyone’s my way. We still live in Futurama today, but it doesn’t feel like utopia. We are locked in a transportation monoculture, reliant on machines that are bad for the planet, bad for the economy, bad for the soul. And, my god, the traffic.

What the hell happened to the future? And how do we stop it from happening again?

Futurama was the creation of Norman Bel Geddes, a Michigan-born designer who started his career building theater sets. By the 1930s, he was leading a field now called industrial design, and his ambition stretched beyond Broadway. Bel Geddes was always looking to solve interesting problems, and when his design firm was between contracts, he would give him employees theoretical problems to keep them busy. One example: What’s the fastest, most luxurious way to get wealthy passengers from New York to Paris? Another: How to eliminate traffic, an increasingly nasty problem in a country with more and more cars crowding roads designed for wagons?

When Bel Geddes heard the 1939 World’s Fair was coming to Flushing, Queens, he spied a stage bigger than any theater’s. And he knew the traffic problem—everyone hates traffic—would bring him his audience. He would fix America’s roadways for the age of the automobile.

Bel Geddes cajoled General Motors into funding the exhibit, and in an 11-month sprint vividly recounted by Barbara Alexandra Szerlip in The Man Who Designed the Future: Norman Bel Geddes and the Invention of Twentieth-Century America, built something no one had seen before. Fair goers who braved the line—sometimes a mile long—would sit on a train of 552 chairs. Each seat had a built-in speaker through which a narrator explained how “this wonderworld of 1960” had eliminated car crashes and congestion with a transcontinental network of cleverly designed highways. Riders would gaze down on that world, marveling at the dioramas of cities dotted by skyscrapers, elevated walkways, and logically placed parks, the cloverleafs that did away with intersections, the networks that let cars coast without interruption.

Over the two years of the New York World’s Fair, close to 30 million people took the ride and walked away with a pin reading “I Have Seen the Future.” Many more heard about the exhibit secondhand, or through radio reports. Perhaps most stunning, Futurama drew more visitors than the Fair’s Midway section, home of amusements like “Miss Nude of 1939” and the burlesque routine of Rosita Royce, whose trained birds removed her clothes.

The Fair came on the heels of the Great Depression and amidst the early days of the Second World War. (Between the 1939 and 1940 seasons, the pavilions put on by Albania, Poland, and Yugoslavia, among others, disappeared.) In the US, it marked a moment when “people were ready for a new vision of prosperity, of a new America,” says Henry Jenkins, a media scholar at the University of Southern California. It was also a moment when science fiction was first entering the cultural mainstream, and with it technological utopianism—the belief that scientific advances could only make life better.

Bel Geddes didn’t invent this idea of the future himself. “Much of Futurama was a pastiche of existing theories and concepts that had appeared in everything from H. G. Wells’s stories and Fritz Lang’s Metropolis to sketches by F. L. Wright and Raymond Hood. And certainly Le Corbusier was in the mix,” Szerlip writes. But it was Bel Geddes and his ride that brought such thinking to the attention of the masses. It was the world of Futurama that took hold.

During the war years, Futurama was put on pause. The production of civilian cars was stopped until 1945, and the resources demanded by a global conflict nixed any thought of major infrastructure work at home. But eventually, the American soldiers came home to a country that had been through more than a decade of deprivation and sacrifice. A sudden superpower, the US was ready to make real that memory of the future.

Car sales boomed. The suburbs flourished, offering an American dream to middle and upper classes that still tempts us today: home ownership, 2.5 kids, prosperity. Highways stretched across the country and bored through urban cores, often devastating vibrant but working-class, usually minority neighborhoods: the South Bronx, Minneapolis’ Rondo, Detroit’s Paradise Valley. As the car monoculture took root, public transportation shriveled, streetcar tracks were torn up. Those who couldn’t afford to buy and keep a car were left with the bus, or their feet. And the traffic was insufferable as ever, as the law of induced demand filled every new square foot of concrete nearly as quick as it was poured.

Yet even before master builder Robert Moses declared “the postwar highway era is here”—in the immediate aftermath of the fighting—some critics had started to resist the tide, at least in New York. Moses was an early example of the deep state, a never-elected bureaucrat who amassed so much power that he dictated how New York built its infrastructure for much of the mid-20th century—and how it’s shaped today. Chief among those who dared challenge him was Lewis Mumford, who railed against New York’s elevation of individual transportation.

“Because we have apparently decided that the private motorcar has a sacred right to go anywhere, halt anywhere, and remain anywhere as long as its owner chooses, we have neglected other means of transportation,” Mumford wrote in The New Yorker in 1955. “The major corrective for this crippling overspecialization is to redevelop now despised modes of circulation—public vehicles and private feet,” an argument common today among 21st century urbanists.

Such warnings proved futile, partly because Moses had nearly complete control over what got funded and built in New York, and he believed in the car above any sort of public transit. (To truly understand today’s cities, take a sabbatical and read Robert Caro’s epic biography of Moses, The Power Broker.)

One man cannot take all the blame. One corporation, though, just might. The ride that wowed millions at the 1939 World’s Fair represented just one strain of the era’s technological utopianism, says Jenkins. The future conjured by H. G. Wells in his book The Shape of Things to Come, and its film adaptation, directed by William Cameron Menzies, included cities full of pedestrians and shared transport.

But Futurama, however artistic, was ultimately a commercial paid for by General Motors. In Szerlip"s telling, Bel Geddes first pitched a similar idea to Shell, and he convinced GM executives to fund his project by telling them the point was to sell not any particular model car, but the future—“With the promise that every citizen can own a piece of that future for the price of a General Motors automobile.”

“We have a corporately sponsored remaking of the technological utopianism through Futurama,” Jenkins says. And that’s the future that we built.

Six decades on, we have a fresh chance. The simultaneous advent of electric, autonomous, and even tubular transportation is an opportunity to rethink and remake our cities. Thus, the renderings, and the promises from companies that before long, the tech they’re developing will clear the air, save lives, and of course, end traffic.

"Highways are an impressive, flashy thing to build. No one is against highways,” Lewis Mumford wrote more than half a century ago. Today, you could swap “hyperloop” for “highway” and you get the same idea—that the shiny future, however ill-conceived, is the one for us.

We have the tools to make sure we don’t repeat our mistakes. “The problem we have now is there is no choice,” says Daniel Sperling, who researches transportation planning at the University of California, Davis. Most places in America, you have to own a car. Autonomous vehicles could change that, and bring mobility to millions. But for the sake of the planet and our lungs, regulators should insist they be electric. To prevent a world where the streets are still clogged with cars, half of them empty, Sperling says, “We desperately need them to be pooled.”

And you can’t settle on one vision, says Di-Ann Eisnor, the director of growth at Waze, who runs the company’s Connected Citizens program. The last time around, “We made assumptions about capacity”—like that you could always make more roads for more cars. Clawing that urban space back demands an experimental mindset. Cities around the world are trying new things. San Francisco is adjusting parking prices based on demand. Mexico City is battling congestion by killing parking. Washington, DC is trying out special zones where Uber and Lyft can safely scoop up passengers. “Technology and community need to go hand in hand,” Eisnor says. “Everyday, test something new.”

Ultimately, we need a future fueled by many imagined utopias, a diversity of approaches and policies. By definition, the monoculture won’t work for all. In the 20th century, the working class was left behind. Any of those lovely renderings would be a fine way to whoosh forward—as long as this time, they bring everyone along for the traffic-free ride.

The future, according to the folks who make the renderings, will be built mostly around whooshing. The details differ from one imagined utopia to the next, but the broad strokes are the same. Cars will run on electricity, drive themselves, even fly. Networks of vacuum tubes and tunnels will connect cities to each other and to the hinterlands. Supersonic jets will turn transoceanic journeys into river crossings. The burning of fossil fuels will seem as remote and unsavory as human sacrifice. Trees will blanket the urban centers; the air will refresh our lungs instead of blackening them.

Moving about the planet will be faster, safer, easier, comfier, greener, cheaper, and whooshier. Best of all, there will be no traffic.

So say the renderings, of which there are many. They’re created by all the players who imagine themselves profitably managing this future—Elon Musk chief among them, but also Lyft and Uber, Ford and General Motors, and innumerable startups.

Ford—which now calls itself a mobility company as well as an automaker—is among the many companies pitching a new, utopian vision of the future.

FOrd

Americans have been given a glimpse of this sort of transportation paradise before. They stood under the hot sun for hours at a time to see it, because they were fed up with traffic, and any world that promises to end it is worth a look. And so millions of people made it up a winding ramp and into a mysterious building and sat in the navy blue mohair chairs that would ferry them through the marquee exhibit of the 1939 New York World’s Fair.

The progenitor of the optimism-soaked hybrid of amusement park and educational diorama later perfected by Walt Disney, Futurama was a 17-minute pitch by General Motors that showed its audience a world that had solved transportation by signing over the ground floor of city and country to the car. Everyone in the picture had the keys to that era’s smartphone, the device that unlocked access to a world of wealth and convenience.

That vision, for the most part, came true. Futurama predicted the world of 1960. By that new decade, the personal car was in fact dominant, suburbs reigned supreme, and the highway was everyone’s my way. We still live in Futurama today, but it doesn’t feel like utopia. We are locked in a transportation monoculture, reliant on machines that are bad for the planet, bad for the economy, bad for the soul. And, my god, the traffic.

What the hell happened to the future? And how do we stop it from happening again?

Futurama was the creation of Norman Bel Geddes, a Michigan-born designer who started his career building theater sets. By the 1930s, he was leading a field now called industrial design, and his ambition stretched beyond Broadway. Bel Geddes was always looking to solve interesting problems, and when his design firm was between contracts, he would give him employees theoretical problems to keep them busy. One example: What’s the fastest, most luxurious way to get wealthy passengers from New York to Paris? Another: How to eliminate traffic, an increasingly nasty problem in a country with more and more cars crowding roads designed for wagons?

When Bel Geddes heard the 1939 World’s Fair was coming to Flushing, Queens, he spied a stage bigger than any theater’s. And he knew the traffic problem—everyone hates traffic—would bring him his audience. He would fix America’s roadways for the age of the automobile.

Bel Geddes cajoled General Motors into funding the exhibit, and in an 11-month sprint vividly recounted by Barbara Alexandra Szerlip in The Man Who Designed the Future: Norman Bel Geddes and the Invention of Twentieth-Century America, built something no one had seen before. Fair goers who braved the line—sometimes a mile long—would sit on a train of 552 chairs. Each seat had a built-in speaker through which a narrator explained how “this wonderworld of 1960” had eliminated car crashes and congestion with a transcontinental network of cleverly designed highways. Riders would gaze down on that world, marveling at the dioramas of cities dotted by skyscrapers, elevated walkways, and logically placed parks, the cloverleafs that did away with intersections, the networks that let cars coast without interruption.

Over the two years of the New York World’s Fair, close to 30 million people took the ride and walked away with a pin reading “I Have Seen the Future.” Many more heard about the exhibit secondhand, or through radio reports. Perhaps most stunning, Futurama drew more visitors than the Fair’s Midway section, home of amusements like “Miss Nude of 1939” and the burlesque routine of Rosita Royce, whose trained birds removed her clothes.

The Fair came on the heels of the Great Depression and amidst the early days of the Second World War. (Between the 1939 and 1940 seasons, the pavilions put on by Albania, Poland, and Yugoslavia, among others, disappeared.) In the US, it marked a moment when “people were ready for a new vision of prosperity, of a new America,” says Henry Jenkins, a media scholar at the University of Southern California. It was also a moment when science fiction was first entering the cultural mainstream, and with it technological utopianism—the belief that scientific advances could only make life better.

Bel Geddes didn’t invent this idea of the future himself. “Much of Futurama was a pastiche of existing theories and concepts that had appeared in everything from H. G. Wells’s stories and Fritz Lang’s Metropolis to sketches by F. L. Wright and Raymond Hood. And certainly Le Corbusier was in the mix,” Szerlip writes. But it was Bel Geddes and his ride that brought such thinking to the attention of the masses. It was the world of Futurama that took hold.

During the war years, Futurama was put on pause. The production of civilian cars was stopped until 1945, and the resources demanded by a global conflict nixed any thought of major infrastructure work at home. But eventually, the American soldiers came home to a country that had been through more than a decade of deprivation and sacrifice. A sudden superpower, the US was ready to make real that memory of the future.

Car sales boomed. The suburbs flourished, offering an American dream to middle and upper classes that still tempts us today: home ownership, 2.5 kids, prosperity. Highways stretched across the country and bored through urban cores, often devastating vibrant but working-class, usually minority neighborhoods: the South Bronx, Minneapolis’ Rondo, Detroit’s Paradise Valley. As the car monoculture took root, public transportation shriveled, streetcar tracks were torn up. Those who couldn’t afford to buy and keep a car were left with the bus, or their feet. And the traffic was insufferable as ever, as the law of induced demand filled every new square foot of concrete nearly as quick as it was poured.

Yet even before master builder Robert Moses declared “the postwar highway era is here”—in the immediate aftermath of the fighting—some critics had started to resist the tide, at least in New York. Moses was an early example of the deep state, a never-elected bureaucrat who amassed so much power that he dictated how New York built its infrastructure for much of the mid-20th century—and how it’s shaped today. Chief among those who dared challenge him was Lewis Mumford, who railed against New York’s elevation of individual transportation.

“Because we have apparently decided that the private motorcar has a sacred right to go anywhere, halt anywhere, and remain anywhere as long as its owner chooses, we have neglected other means of transportation,” Mumford wrote in The New Yorker in 1955. “The major corrective for this crippling overspecialization is to redevelop now despised modes of circulation—public vehicles and private feet,” an argument common today among 21st century urbanists.

Such warnings proved futile, partly because Moses had nearly complete control over what got funded and built in New York, and he believed in the car above any sort of public transit. (To truly understand today’s cities, take a sabbatical and read Robert Caro’s epic biography of Moses, The Power Broker.)

One man cannot take all the blame. One corporation, though, just might. The ride that wowed millions at the 1939 World’s Fair represented just one strain of the era’s technological utopianism, says Jenkins. The future conjured by H. G. Wells in his book The Shape of Things to Come, and its film adaptation, directed by William Cameron Menzies, included cities full of pedestrians and shared transport.

But Futurama, however artistic, was ultimately a commercial paid for by General Motors. In Szerlip"s telling, Bel Geddes first pitched a similar idea to Shell, and he convinced GM executives to fund his project by telling them the point was to sell not any particular model car, but the future—“With the promise that every citizen can own a piece of that future for the price of a General Motors automobile.”

“We have a corporately sponsored remaking of the technological utopianism through Futurama,” Jenkins says. And that’s the future that we built.

Six decades on, we have a fresh chance. The simultaneous advent of electric, autonomous, and even tubular transportation is an opportunity to rethink and remake our cities. Thus, the renderings, and the promises from companies that before long, the tech they’re developing will clear the air, save lives, and of course, end traffic.

"Highways are an impressive, flashy thing to build. No one is against highways,” Lewis Mumford wrote more than half a century ago. Today, you could swap “hyperloop” for “highway” and you get the same idea—that the shiny future, however ill-conceived, is the one for us.

We have the tools to make sure we don’t repeat our mistakes. “The problem we have now is there is no choice,” says Daniel Sperling, who researches transportation planning at the University of California, Davis. Most places in America, you have to own a car. Autonomous vehicles could change that, and bring mobility to millions. But for the sake of the planet and our lungs, regulators should insist they be electric. To prevent a world where the streets are still clogged with cars, half of them empty, Sperling says, “We desperately need them to be pooled.”

And you can’t settle on one vision, says Di-Ann Eisnor, the director of growth at Waze, who runs the company’s Connected Citizens program. The last time around, “We made assumptions about capacity”—like that you could always make more roads for more cars. Clawing that urban space back demands an experimental mindset. Cities around the world are trying new things. San Francisco is adjusting parking prices based on demand. Mexico City is battling congestion by killing parking. Washington, DC is trying out special zones where Uber and Lyft can safely scoop up passengers. “Technology and community need to go hand in hand,” Eisnor says. “Everyday, test something new.”

Ultimately, we need a future fueled by many imagined utopias, a diversity of approaches and policies. By definition, the monoculture won’t work for all. In the 20th century, the working class was left behind. Any of those lovely renderings would be a fine way to whoosh forward—as long as this time, they bring everyone along for the traffic-free ride.

TORONTO (Reuters) - Facebook Inc plans to open an artificial-intelligence laboratory in Montreal, which will be run by prominent AI researcher Joelle Pineau, two people familiar with the plan said on Friday. Tech

Earlier this year, WIRED published a story that asked a question that seemed to encapsulate internet culture in 2017: What does "covfefe" mean? The nonsense term was tweeted out by President Donald Trump, and the internet went into a fit trying to define it. As WIRED culture writer Angela Watercutter wrote, "Nearly every great meme starts with an obscure word, hashtag, or image that is then granted humor based on what the internet does with it. "On fleek," "Damn, Daniel," Kermit sipping tea—all of these things have meanings given to them by people online. In fact, creating and spreading new language is one of social media"s greatest skill sets."

Free web hosting can be very enticing to individuals and businesses that do not have enough money to afford good web hosting services. But is it something worth the time spent and efforts done?

Fortunately there are proven ways on how to determine the most suited web host for your requirements. First you have to do an extensive research. Gather as many information on free web hosting services. You can always do this by doing an online search at google or yahoo.

After compiling your list then decide the service that you want from a web host. Consider the advantages and disadvantages of availing the services of a particular web host. You might also want to ask around. Actually there are a lot of discussion forums on the Internet regarding free website hosting. Go around discussion boards and read. You can also ask people who have availed of free website hosting about their experiences in getting a free hosting service. This is a good way for you to learn about the pros as well as cons of getting such service.

Free web hosting also gave its users with sub domain name, making it almost impossible to be searched on in various search engines. This made most websites on free web host servers almost impossible to be found on search engines. Reliability was also a concern, troubling most business owners who availed of free website hosting. With all these problems arising, there"s little doubt that getting free website hosting is not that practical. It will not help websites particularly those selling products and services.

Remember, every free hosting firm will try to make money from your website. Look for a hosting firm, which is less intrusive and more reliable.

About the Author:

Learn more about dedicated hosting web and get a Free limited report on Web Hosting Insights, a popular website that provides free tips and advice on web hosting solutions.

TORONTO (Reuters) - Facebook Inc plans to open an artificial-intelligence laboratory in Montreal, which will be run by prominent AI researcher Joelle Pineau, two people familiar with the plan said on Friday. Tech

Free web hosting can be very enticing to individuals and businesses that do not have enough money to afford good web hosting services. But is it something worth the time spent and efforts done?

Fortunately there are proven ways on how to determine the most suited web host for your requirements. First you have to do an extensive research. Gather as many information on free web hosting services. You can always do this by doing an online search at google or yahoo.

After compiling your list then decide the service that you want from a web host. Consider the advantages and disadvantages of availing the services of a particular web host. You might also want to ask around. Actually there are a lot of discussion forums on the Internet regarding free website hosting. Go around discussion boards and read. You can also ask people who have availed of free website hosting about their experiences in getting a free hosting service. This is a good way for you to learn about the pros as well as cons of getting such service.

Free web hosting also gave its users with sub domain name, making it almost impossible to be searched on in various search engines. This made most websites on free web host servers almost impossible to be found on search engines. Reliability was also a concern, troubling most business owners who availed of free website hosting. With all these problems arising, there"s little doubt that getting free website hosting is not that practical. It will not help websites particularly those selling products and services.

Remember, every free hosting firm will try to make money from your website. Look for a hosting firm, which is less intrusive and more reliable.

About the Author:

Learn more about dedicated hosting web and get a Free limited report on Web Hosting Insights, a popular website that provides free tips and advice on web hosting solutions.

TORONTO (Reuters) - Facebook Inc plans to open an artificial-intelligence laboratory in Montreal, which will be run by prominent AI researcher Joelle Pineau, two people familiar with the plan said on Friday. Tech

The tax reform package that recently passed through Congress has major implications for investors. The tax plan is a major piece of legislation that will directly benefit large U.S. corporations, such as those that comprise the S&P 500. There are many components of the bill, perhaps the most significant of which is a permanent lowering of the corporate tax rate, from 35% to 21%.

A sharply lower corporate tax rate is a huge tailwind for large companies. Specifically, the retail industry is set to benefit, as many large U.S. retailers carry tax rates of 30%+. Meaningfully lower tax bills could result in much greater earnings to be distributed to shareholders, in the form of share repurchases and dividends.

With that in mind, we have identified 3 dividend-paying retail stocks that should benefit greatly from tax reform.

As previously mentioned, less money paid in taxes means more money available for shareholder distributions. Therefore, Target is an ideal choice for this list, because it is already a Dividend Aristocrat, which have increased their dividends for 25+ consecutive years You can see all 51 Dividend Aristocrats here.

Target has paid 200 quarterly dividends in a row, and has increased its dividend for 46 consecutive years. A corporate tax rate of 21% would greatly improve Target’s bottom line, since the company had an effective tax rate of 32%, according to ValueLine.

Target has had to spend aggressively to fight off online retail competition, led by Amazon (AMZN). As a result, Target’s earnings-per-share declined 6.2% over the first three quarters of 2017. The good news is, Target has surpassed analyst expectations for both revenue and earnings-per-share, in all three quarters to start the year. In the most recent quarter, Target’s comparable store sales increased 0.9%, while traffic rose 1.4%.

Target has launched several initiatives to return to growth. First, it is in the process of redeveloping hundreds of stores. To do this, it is modernizing layouts, and adding new product categories.

Target expects it can achieve a 2%-4% lift in sales for each store it renovates. By 2018, the company expects to have completed reimagining on over 350 of its stores. By 2019, it will have reimagined over 600 stores, representing one-third of its total store count.

Another major growth catalyst for Target is its small stores, under the CityTarget and TargetExpress banners. These are stores with much less square footage, in places that cannot provide the necessary space to build a large store, such as urban areas and college campuses.

By 2019, Target expects to open over 100 small stores, triple the number of small stores currently in operation.

Lastly, Target building its own e-commerce platform. Target’s comparable digital sales increased 24% last quarter. Target expanded its next-day delivery of essential items to eight new U.S. cities. And, Target recently acquired Shipt for $550 million in cash. Shipt is a same-day delivery service that will help Target improve its digital fulfillment, and compete better with Amazon.

Target has a secure dividend, with a 55% payout ratio using expected 2017 earnings. Its turnaround initiatives should return the company to growth, aided by tax reform. That means Target should have little trouble maintaining its Dividend Aristocrat status moving forward.

Macy’s stock has declined approximately 30% year-to-date. This is no doubt a difficult period for Macy’s, but it has been through many ups and downs during its history. Macy’s has been in business since 1858. The combination of more than 100+ years in business, and a 3%+ dividend yield, earns Macy’s a spot on our list of “blue-chip” stocks. You can see our entire list of blue chip stocks here.

But with high dividend yield and low valuation, Macy’s could be a value and income opportunity for 2018. Macy’s declining share price has elevated its dividend yield to 6%. We believe stocks with 5%+ dividend yields to be especially attractive yields for income investors. You can see our entire list of all 397 stocks with 5%+ dividend yields here.

Macy’s would be a huge winner from tax reform, as it has a tax rate of 37% according to ValueLine. As a result, tax reform would be a major boost to Macy’s bottom line, and it could not come at a better time for the company. Department stores like Macy’s have been among the hardest-hit companies by the rise of e-commerce. In turn, Macy’s has had to invest huge sums of money into its core turnaround initiatives.

Macy’s earnings-per-share declined 38% in 2016. Over the first three quarters, adjusted earnings-per-share declined another 14%. For 2017, management expects comparable sales to decline 2% to 3%. However, the declines have slowed throughout 2017, which potentially positions Macy’s to return to growth next year.

Macy’s Backstage and Bluemercury stores are compelling growth catalysts. Last quarter, Macy’s opened eight new freestanding Bluemercury stores, bringing the total to 135. It also opened seven new Macy’s Backstage stores within existing Macy’s, and how has 45 locations. These store openings will help Macy’s expand in the beauty and off-price channels, which are growing categories.

In addition, Macy’s has a huge amount of real estate value on the balance sheet. Activist investor Starboard Value once pegged Macy’s real estate value at more than $20 billion. Starboard is no longer an investor, but even if its valuation was too aggressive, Macy’s could still be a bargain. The company has a current enterprise value of just $13.5 billion.

Macy’s annualized dividend payout of $1.51 represents a payout ratio of 48% to 52%, based on 2017 earnings guidance. As a result, Macy’s is appealing for value, and income.

Kohl’s has an attractive dividend yield slightly above 4%. Kohl’s is one of 674 stocks in the consumer cyclical sector that pays a dividend. You can see our list of all 674 dividend-paying consumer cyclical stocks here.

Like Macy’s, Kohl’s has a high tax rate, of 37.5%, which means it would also be a huge winner from a significantly lower tax rate. Kohl’s bottom line could use a boost—earnings-per-share declined by 10% in 2016.

Kohl’s has implemented several initiatives to restore growth, which appear to be gaining traction. With regard to Amazon, Kohl’s seems to have adopted a policy of “if you can’t beat ‘em, join ‘em.” In October, Kohl’s announced it will dedicate roughly 1,000 square feet inside its stores for Amazon smart-home spaces.

In these areas, consumers can purchase Amazon devices, such as the Echo and Fire tablets, along with accessories and smart home devices and services, directly from Amazon. The program initially launched in 10 stores, in Los Angeles and Chicago.

In addition, Kohl’s added Under Armour (UA) products to its active and wellness category earlier this year. This helped Kohl’s by adding one of the most popular brands, in a growth category.

As a result, Kohl’s results have improved over the course of 2017. Comparable sales declined 1% over the first three quarters of 2017, but this was far better than the 2.4% decline in the same nine-month period in 2016. Adjusted earnings-per-share were flat in the first three quarters of 2017. For the full year, Kohl’s expects adjusted earnings-per-share of $3.60 to $3.80, which easily covers the annualized dividend of $2.20.

Final Thoughts

Target, Macy’s, and Kohl’s all have dividend yields ranging from 3%-6%.

And, they all appear to be undervalued. They all have price-to-earnings ratios is the low teens. Investors became much more pessimistic toward these retailers over the past year, due to the intense competitive threats facing brick-and-mortar retailers.

However, Target, Macy’s, and Kohl’s are still highly profitable, and can easily cover their hefty dividends. Plus, they are each implementing strategic initiatives to return to growth moving forward. Tax reform could be just the catalyst needed to improve their valuations and earnings growth.

Looking for value stocks with even longer histories of dividend increases? Our service Undervalued Aristocrats provides actionable buy and sell recommendations on some of the most undervalued dividend growth stocks around.Click here to learn more.

Disclosure:I am/we are long TGT, M.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

As we explained in Part 1, the most dangerous place on the planet financially is now the Wall Street casino. In the months ahead, it will become ground zero of the greatest monetary/fiscal collision in recorded history.

For the first time ever both the Fed and the US treasury will be dumping massive amounts of public debt on the bond market---upwards of $1.8 trillion between them in FY 2019 alone---and at a time which is exceedingly late in the business cycle. That double whammy of government debt supply will generate a thundering "yield shock" which, in turn, will pull the props out from under equity and other risk asset markets----all of which have "priced-in" ultra low debt costs as far as the eye can see.

The anomalous and implicitly lethal character of this prospective clash can not be stressed enough. Ordinarily, soaring fiscal deficits occur early in the cycle. That is, during the plunge unto recession, when revenue collections drop and outlays for unemployment benefits and other welfare benefits spike; and also during the first 15-30 months of recovery, when Keynesian economists and spendthrift politicians join hands to goose the recovery----not understanding that capitalist markets have their own regenerative powers once the excesses of bad credit, malinvestment and over-investment in inventory and labor which triggered the recession have been purged.

By contrast, the Federal deficit is now soaring at the tail end (month #102) of an aging business expansion. And the cause is not the exogenous effects of so-called automatic fiscal stabilizers associated with a macroeconomic downturn, but deliberate Washington policy decisions made by the Trumpian GOP.

During FY 2019, for example, these discretionary plunges into deficit finance include slashing revenue by $280 billion, while pumping up an already bloated baseline spending level of $4.375 trillion by another $200 billion for defense, disasters, border control, ObamaCare bailouts and domestic pork barrel of every shape and form.

These 11th hour fiscal maneuvers, in fact, are so asinine that the numbers have to be literally seen to be believed. To wit, an already weak-growth crippled revenue baseline will be cut to just $3.4 trillion, while the GOP spenders goose outlays toward the $4.6 trillion mark.

That"s right. Nine years into a business cycle expansion, the King of Debt and his unhinged GOP majority on Capitol Hill have already decided upon (an nearly implemented) the fiscal measures that will result in borrowing 26 cents on every dollar of FY 2019 spending. JM Keynes himself would be grinning with self-satisfaction.

Moreover, this foolhardy attempt to re-prime-the-pump nearly a decade after the Great Recession officially ended means that monetary policy is on its back foot like never before.

What we mean is that both Bernanke and Yellen were scared to death of the tidal waves of speculation that their money printing policies of QE and ZIRP had fostered in the financial markets. So once the heat of crisis had clearly passed and the market had recovered its pre-crisis highs in early 2013, they nevertheless deferred, dithered and procrastinated endlessly on normalization of interest rates and the Fed"s elephantine balance sheet.

So what we have now is a central bank desperately trying to recapture lost time via its "automatic pilot" commitment to systematic and sustained balance sheet shrinkage at fixed monthly dollar amounts. This unprecedented "quantitative tightening" or QT campaign has already commenced at $1o billion of bond sales per month (euphemistically described as "portfolio run-off" by the Eccles Building) during the current quarter and will escalate automatically until it reaches $50 billion per month ($600 billion annualized) next October .

Needless to say, that"s the very opposite of the "accommodative" Fed posture and substantial debt monetization which ordinarily accompanies an early-cycle ballooning of Uncle Sam"s borrowing requirements. And the present motivation of our Keynesian monetary central planners is even more at variance with the normal cycle.

To wit, they plan to stick with QT come hell or high water because they are in the monetary equivalent of a musket reloading mode. Failing to understand that the main street economy essentially recovered on its own after the 2008-2009 purge of the Greenspanian excesses (and that"s its capacity to rebound remains undiminished), the Fed is desperate to clear balance sheet headroom and regain interest rate cutting leverage so that it will have the wherewithal to "stimulate" the US economy out of the next recession.

Needless to say, this kind of paint-by-the-numbers Keynesianism is walking the whole system right into a perfect storm. When the GOP-Trumpian borrowing bomb hits the bond market next October we will already be in month #111 of the current expansion cycle and as the borrowing after-burners kick-in during the course of the year, FY 2019 will close out in month #123.

Here"s the thing. The US economy has never been there before. Never in the recorded history of the republic has a business expansion lasted 123 months. During the post-1950 period shown below, the average expansion has been only 61 months and the two longest ones have their own disabilities.

The 105 month expansion during the 1960s was fueled by LBJ"s misbegotten "guns and butter" policies and ended in the dismal stagflation of the 1970s. And the 119 month expansion of the 1990s reflected the Greenspan fostered household borrowing binge and tech bubbles that fed straight into the crises of 2008-2009.

Yet the Trumpian-GOP has not only presumed to pump-up the fiscal deficit to 6.2% of GDP just as the US economy enters the terra incognito range of the business cycle (FY 2019); it has actually declared its virtual abolition. Ironically, in fact, on December 31, 2025 nearly all of the individual income cuts expire----meaning that in FY 2026 huge tax increases will smack the household sector at a $200 billion run-rate!

But not to worry. The GOP"s present-day fiscal geniuses insist that the current business expansion, which will then be 207 months old, will end up no worse for the wear. The public debt will then total $33 trillion or 130% of GDP---even as the US economy gets monkey-hammered by huge tax increase.

Alas, no harm, no foul. The business expansion is presumed to crank forward through FY 2027 or month #219.

Needless to say, the whole thing degenerates into a sheer fiscal and economic fairy-tale when you examine the data and projections. But that hasn"t deterred the GOP"s fiscal dreamers.

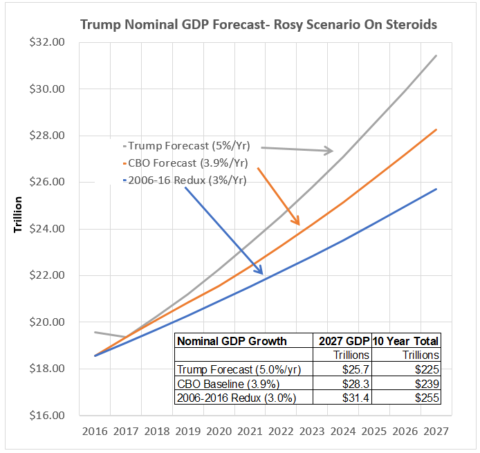

Not only have they implicitly embraced an out-of-this-word 219 month business cycle expansion, but they have also insisted it will unfold at an average nominal GDP growth rate that has not been remotely evident at any time during the 21st century.

As shown in the chart below, the 10-year CBO forecast of nominal GDP (yellow line) is already quite optimistic relative to where GDP would print under the actual growth rate of the last ten-years (blue line). In fact, the CBO forecast generates $16 trillion of extra GDP and nearly $3 trillion more Federal revenue than would a replay of the last 10-years---and notwithstanding the massive fiscal and monetary stimulus during that period.

Still, the GOP/Trump forecast (grey line) assumes a full percentage point of higher GDP growth on top of CBO and no intervening recession and resulting GDP relapse.

Accordingly, the GOP assumes $30 trillion of extra GDP over the coming decade or nearly 23%more than would be generated by the actual growth rate (blue line) of the last decade; and consequently, $6 trillion of extra revenue.

That"s right. An already geriatric business cycle is going t0 rear-up on its hind legs and take off into a new phase of growth in the face of an epochal pivot of monetary policy to QT and a public debt burden relative to GDP that is approaching a Greek-style end game.

(Note: Figures in the box are inverted. First line should be 2006-2012 redux and third line should be Trump forecast.)

Stated differently, fiscal policy has descended into the hands of political mad-men at the very time that monetary policy is inexorably slouching toward normalization. Under those circumstances there is simply no way of avoiding the "yield shock" postulated above, and the cascading "reset" of financial asset prices that it will trigger across the length and breadth of the financial system.

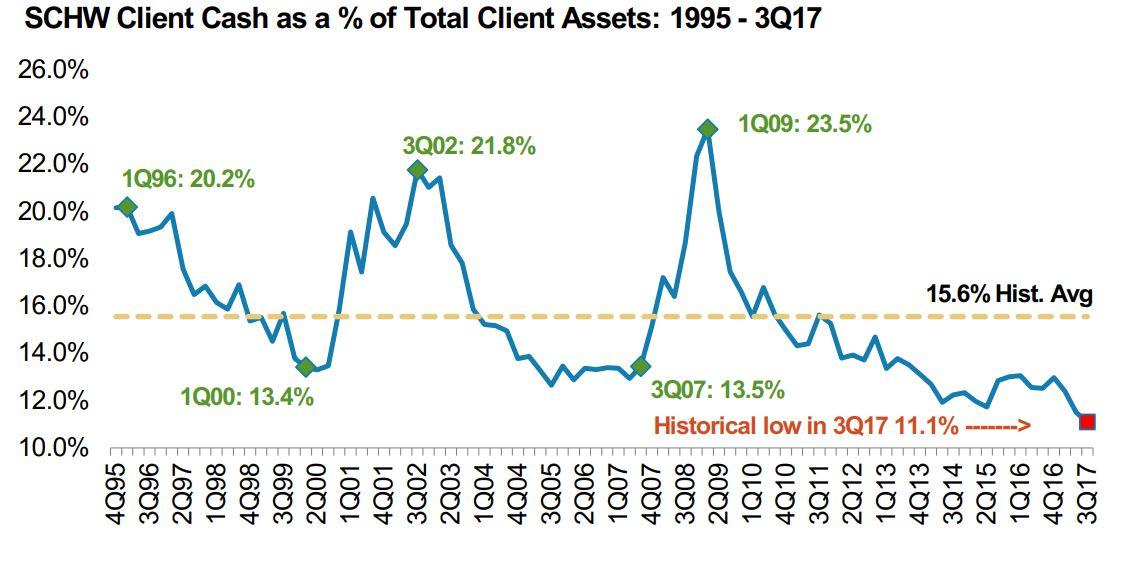

As usual, however, the homegamers are the last to get the word. The unaccountable final spasm of the stock market in 2017 will undoubtedly come to be seen as the last call of the sheep to the slaughter. And owing to the speculative mania that has been fostered by the Fed and its fellow-traveling central banks, it now appears that the homegamers are all-in for the third time since 1987.

Indeed, Schwab"s retail clients have never, ever had lower cash allocations than at the present time---not even during the run-up to the dotcom bust or the great financial crisis.

But this time these predominately baby-boom investors are out of time and on the cusp of retirement---if not already living on one of the Donald"s golf resorts. When the crash comes they will have no opportunity to recover----nor will Washington have the wherewithal to stimulate another phony facsimile of the same.

The GOP-Trumpian gang has already blown their wad on fiscal policy and the Fed is stranded high and dry still close the zero-bound and still saddled with an elephantine balance sheet.

That is, what is fundamentally different about the greatest financial bubble yet is that there is no possibility of a quick policy-induced reflation after the coming crash. This time the cycle will be L-shaped----- with financial asset prices languishing on the post-crash bottom for years to come.

And that is a truly combustible condition. That is, 65% of the retirement population already lives essentially hand-to-month on social security, Medicare and other government welfare benefits (food stamps and SSI, principally). But after the third financial bubble of this century crashes, tens of millions more will be driven close to that condition as their 401Ks again evaporate.

That"s why the fiscal game being played by the Donald and his GOP confederates is so profoundly destructive. Now is the last time to address the entitlement monster, but they have decided to throw fiscal caution to the winds and borrow upwards of $1.6 trillion (with interest) to enable US corporations to fund a new round of stock buybacks, dividend increases and feckless, unproductive M&A deals.

Then again, what the GOP has not forgotten is the care and feeding of its donor class. That mission is being accomplished handsomely as it fills up the deep end of the Swamp with pointless, massive defense spending increases and satisfies K-Street with a grotesquely irresponsible tax bill that was surely of the lobbies, by the PACs and for the money.

At the end of the day, however, the laws of free markets and sound finance will out. The coming crash of the greatest bubble ever will prove that in spades.

As we explained in Part 1, the most dangerous place on the planet financially is now the Wall Street casino. In the months ahead, it will become ground zero of the greatest monetary/fiscal collision in recorded history.

For the first time ever both the Fed and the US treasury will be dumping massive amounts of public debt on the bond market---upwards of $1.8 trillion between them in FY 2019 alone---and at a time which is exceedingly late in the business cycle. That double whammy of government debt supply will generate a thundering "yield shock" which, in turn, will pull the props out from under equity and other risk asset markets----all of which have "priced-in" ultra low debt costs as far as the eye can see.

The anomalous and implicitly lethal character of this prospective clash can not be stressed enough. Ordinarily, soaring fiscal deficits occur early in the cycle. That is, during the plunge unto recession, when revenue collections drop and outlays for unemployment benefits and other welfare benefits spike; and also during the first 15-30 months of recovery, when Keynesian economists and spendthrift politicians join hands to goose the recovery----not understanding that capitalist markets have their own regenerative powers once the excesses of bad credit, malinvestment and over-investment in inventory and labor which triggered the recession have been purged.

By contrast, the Federal deficit is now soaring at the tail end (month #102) of an aging business expansion. And the cause is not the exogenous effects of so-called automatic fiscal stabilizers associated with a macroeconomic downturn, but deliberate Washington policy decisions made by the Trumpian GOP.

During FY 2019, for example, these discretionary plunges into deficit finance include slashing revenue by $280 billion, while pumping up an already bloated baseline spending level of $4.375 trillion by another $200 billion for defense, disasters, border control, ObamaCare bailouts and domestic pork barrel of every shape and form.

These 11th hour fiscal maneuvers, in fact, are so asinine that the numbers have to be literally seen to be believed. To wit, an already weak-growth crippled revenue baseline will be cut to just $3.4 trillion, while the GOP spenders goose outlays toward the $4.6 trillion mark.

That"s right. Nine years into a business cycle expansion, the King of Debt and his unhinged GOP majority on Capitol Hill have already decided upon (an nearly implemented) the fiscal measures that will result in borrowing 26 cents on every dollar of FY 2019 spending. JM Keynes himself would be grinning with self-satisfaction.

Moreover, this foolhardy attempt to re-prime-the-pump nearly a decade after the Great Recession officially ended means that monetary policy is on its back foot like never before.

What we mean is that both Bernanke and Yellen were scared to death of the tidal waves of speculation that their money printing policies of QE and ZIRP had fostered in the financial markets. So once the heat of crisis had clearly passed and the market had recovered its pre-crisis highs in early 2013, they nevertheless deferred, dithered and procrastinated endlessly on normalization of interest rates and the Fed"s elephantine balance sheet.

So what we have now is a central bank desperately trying to recapture lost time via its "automatic pilot" commitment to systematic and sustained balance sheet shrinkage at fixed monthly dollar amounts. This unprecedented "quantitative tightening" or QT campaign has already commenced at $1o billion of bond sales per month (euphemistically described as "portfolio run-off" by the Eccles Building) during the current quarter and will escalate automatically until it reaches $50 billion per month ($600 billion annualized) next October .

Needless to say, that"s the very opposite of the "accommodative" Fed posture and substantial debt monetization which ordinarily accompanies an early-cycle ballooning of Uncle Sam"s borrowing requirements. And the present motivation of our Keynesian monetary central planners is even more at variance with the normal cycle.

To wit, they plan to stick with QT come hell or high water because they are in the monetary equivalent of a musket reloading mode. Failing to understand that the main street economy essentially recovered on its own after the 2008-2009 purge of the Greenspanian excesses (and that"s its capacity to rebound remains undiminished), the Fed is desperate to clear balance sheet headroom and regain interest rate cutting leverage so that it will have the wherewithal to "stimulate" the US economy out of the next recession.

Needless to say, this kind of paint-by-the-numbers Keynesianism is walking the whole system right into a perfect storm. When the GOP-Trumpian borrowing bomb hits the bond market next October we will already be in month #111 of the current expansion cycle and as the borrowing after-burners kick-in during the course of the year, FY 2019 will close out in month #123.

Here"s the thing. The US economy has never been there before. Never in the recorded history of the republic has a business expansion lasted 123 months. During the post-1950 period shown below, the average expansion has been only 61 months and the two longest ones have their own disabilities.

The 105 month expansion during the 1960s was fueled by LBJ"s misbegotten "guns and butter" policies and ended in the dismal stagflation of the 1970s. And the 119 month expansion of the 1990s reflected the Greenspan fostered household borrowing binge and tech bubbles that fed straight into the crises of 2008-2009.

Yet the Trumpian-GOP has not only presumed to pump-up the fiscal deficit to 6.2% of GDP just as the US economy enters the terra incognito range of the business cycle (FY 2019); it has actually declared its virtual abolition. Ironically, in fact, on December 31, 2025 nearly all of the individual income cuts expire----meaning that in FY 2026 huge tax increases will smack the household sector at a $200 billion run-rate!

But not to worry. The GOP"s present-day fiscal geniuses insist that the current business expansion, which will then be 207 months old, will end up no worse for the wear. The public debt will then total $33 trillion or 130% of GDP---even as the US economy gets monkey-hammered by huge tax increase.

Alas, no harm, no foul. The business expansion is presumed to crank forward through FY 2027 or month #219.

Needless to say, the whole thing degenerates into a sheer fiscal and economic fairy-tale when you examine the data and projections. But that hasn"t deterred the GOP"s fiscal dreamers.

Not only have they implicitly embraced an out-of-this-word 219 month business cycle expansion, but they have also insisted it will unfold at an average nominal GDP growth rate that has not been remotely evident at any time during the 21st century.

As shown in the chart below, the 10-year CBO forecast of nominal GDP (yellow line) is already quite optimistic relative to where GDP would print under the actual growth rate of the last ten-years (blue line). In fact, the CBO forecast generates $16 trillion of extra GDP and nearly $3 trillion more Federal revenue than would a replay of the last 10-years---and notwithstanding the massive fiscal and monetary stimulus during that period.

Still, the GOP/Trump forecast (grey line) assumes a full percentage point of higher GDP growth on top of CBO and no intervening recession and resulting GDP relapse.

Accordingly, the GOP assumes $30 trillion of extra GDP over the coming decade or nearly 23%more than would be generated by the actual growth rate (blue line) of the last decade; and consequently, $6 trillion of extra revenue.

That"s right. An already geriatric business cycle is going t0 rear-up on its hind legs and take off into a new phase of growth in the face of an epochal pivot of monetary policy to QT and a public debt burden relative to GDP that is approaching a Greek-style end game.

(Note: Figures in the box are inverted. First line should be 2006-2012 redux and third line should be Trump forecast.)

Stated differently, fiscal policy has descended into the hands of political mad-men at the very time that monetary policy is inexorably slouching toward normalization. Under those circumstances there is simply no way of avoiding the "yield shock" postulated above, and the cascading "reset" of financial asset prices that it will trigger across the length and breadth of the financial system.

As usual, however, the homegamers are the last to get the word. The unaccountable final spasm of the stock market in 2017 will undoubtedly come to be seen as the last call of the sheep to the slaughter. And owing to the speculative mania that has been fostered by the Fed and its fellow-traveling central banks, it now appears that the homegamers are all-in for the third time since 1987.

Indeed, Schwab"s retail clients have never, ever had lower cash allocations than at the present time---not even during the run-up to the dotcom bust or the great financial crisis.

But this time these predominately baby-boom investors are out of time and on the cusp of retirement---if not already living on one of the Donald"s golf resorts. When the crash comes they will have no opportunity to recover----nor will Washington have the wherewithal to stimulate another phony facsimile of the same.

The GOP-Trumpian gang has already blown their wad on fiscal policy and the Fed is stranded high and dry still close the zero-bound and still saddled with an elephantine balance sheet.

That is, what is fundamentally different about the greatest financial bubble yet is that there is no possibility of a quick policy-induced reflation after the coming crash. This time the cycle will be L-shaped----- with financial asset prices languishing on the post-crash bottom for years to come.

And that is a truly combustible condition. That is, 65% of the retirement population already lives essentially hand-to-month on social security, Medicare and other government welfare benefits (food stamps and SSI, principally). But after the third financial bubble of this century crashes, tens of millions more will be driven close to that condition as their 401Ks again evaporate.

That"s why the fiscal game being played by the Donald and his GOP confederates is so profoundly destructive. Now is the last time to address the entitlement monster, but they have decided to throw fiscal caution to the winds and borrow upwards of $1.6 trillion (with interest) to enable US corporations to fund a new round of stock buybacks, dividend increases and feckless, unproductive M&A deals.

Then again, what the GOP has not forgotten is the care and feeding of its donor class. That mission is being accomplished handsomely as it fills up the deep end of the Swamp with pointless, massive defense spending increases and satisfies K-Street with a grotesquely irresponsible tax bill that was surely of the lobbies, by the PACs and for the money.

At the end of the day, however, the laws of free markets and sound finance will out. The coming crash of the greatest bubble ever will prove that in spades.