I just finished writing my monthly newsletter (Forbes Real Estate Investor), and in the upcoming edition, I decided to provide a special Rhino REIT Portfolio. It’s a new special edition series, and my goal is to help investors build a diversified portfolio of the highest-quality names at the cheapest prices.

In order to construct a truly balanced portfolio, I decided to provide my top picks for all of the property sector and sub-sectors. Over the years, I have found that the key to investing is to diversify such that you can eliminate sector and geographic risks, while also taking advantage of sectors that offer more favorable growth.

I have always been attracted to the Net Lease REIT sector. As many of you know, I was formerly a Net Lease developer, where I built stores for companies such as Advance Auto Parts (NYSE:AAP), O’Reilly Auto Parts (NASDAQ:ORLY), CVS Health (NYSE:CVS), Walgreen’s (NASDAQ:WBA), Blockbuster Video, and Sherwin-Williams (NYSE:SHW).

The free-standing (Net Lease) sector is one of the most reliable and predictable real estate categories, and in 2017, the Net Lease REIT sector outperformed (total return of 5.0%), as the group benefited from the slight decline in 10-year interest rates (compared to 3.6% for REITs in 2017). As I explained in the upcoming newsletter:

“In 2018, we expect fundamentals to remain relatively stable, with potential growth at the high-end of industry averages, fueled by tax reform. Net Lease REITs are historically counter-cyclical, lagging the industry during stronger economic cycles and rising interest rates... we believe that the REITs with the lowest cost of capital will be better equipped to mitigate rate risk.”

Our top Net Lease REIT picks include Realty Income (NYSE:O), STORE Capital (NYSE:STOR), and W.P. Carey (NYSE:WPC). Also, we like the less traditional Net Lease REIT, EPR Properties (NYSE:EPR).

Of course, I did not include in my special “Rhino Report” the list of Net Lease REITs to avoid. We cover a growing list of Equity REITs and Rubicon Associates, and I don’t have the resources to pick the losers. We prefer to focus 100% of our efforts on picking the companies that will outperform.

However, a few days ago, I ran across an article on Seeking Alpha that deserved more than the standard “you should avoid this REIT at all costs” reply. As my following recognizes, I have a fiduciary (adjective: synonym "trusted") responsibility to send a warning call whenever there is potential for elevated risk, and so now you know why I decided to provide “a harbinger warning" for Global Net Lease (NYSE:GNL).

Chapter One: Global Net Lease

First off, I want to thank Dane Bowler for providing high-quality content on Seeking Alpha. I have known Dane for a number of years, and I have great respect for his work. He and I agree on many recommendations, and it’s rare that we disagree - this is one occasion.

Last week, Dane wrote an article titled "Global Net Lease: A Stable 11%+ Dividend Yield And Significant Upside". Here’s his summary:

“GNL is poised to generate a roughly 11% annual return to investors for a long stretch of time or 45% capital appreciation depending on the whims of the market. This return comes with the caveat that fundamentals need to hold up. From a property and tenant standpoint, the fundamentals look fantastic and even superior to those of blue-chip peers. At this deeply discounted market price, we believe the reward significantly outweighs the risk.”

Global Net Lease began trading on June 3, 2015. Formerly American Realty Capital Global Trust, a non-traded REIT, GNL was re-branded (changed its name), but the REIT is being externally managed by AR Global Investments, LLC.

As a result, GNL"s executive officers, advisor and its affiliates face conflicts of interest, including significant conflicts created by the advisor"s compensation arrangements with the U.S. and other investment programs advised by AR Global Investments, LLC"s affiliates and conflicts in allocating time among these investment programs and the U.S. As GNL discloses in its Investor Presentation:

“Because investment opportunities that are suitable for us may also be suitable for other AR Global Investments, LLC advised investment programs, our Advisor and its affiliates face conflicts of interest relating to the purchase of properties and other investments and such conflicts may not be resolved in our favor, which could reduce the investment return to our stockholders.”

As typical of many non-traded REIT listings, GNL launched a tender offer to acquire a maximum of $125 million of its shares of common stock at $10.50 per share. On February 28, 2017, the company completed a 1-for-3 reverse stock split.

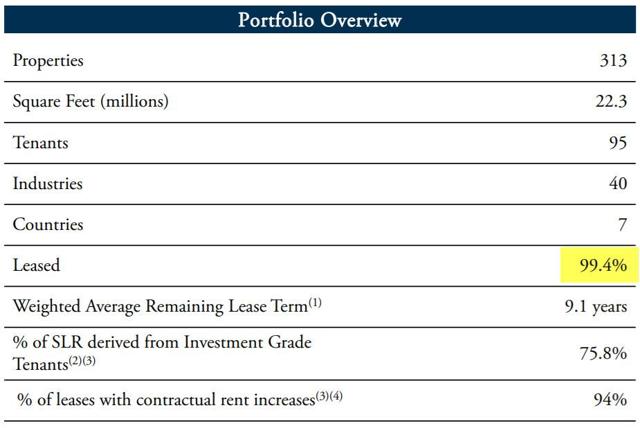

Today, the REIT"s portfolio consists of over 313 Net Lease properties and around 22.3 million square feet. The overall portfolio occupancy is 99.4% leased.

Many of its US properties were acquired in 2013 and 2014, when ARCT and Cole Capital were also aggressively acquiring Net Lease properties. GNL has 94 tenants doing business in 40 industries.

In its Investor Presentation, the company states that its investments are "mission critical assets that are strategically important to tenants’ core operating businesses." The portfolio"s top ten tenants represent 40% of SLR:

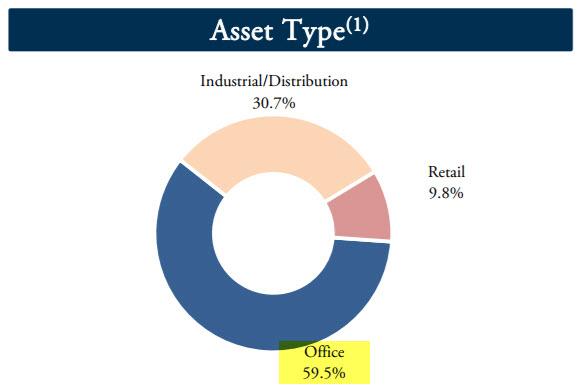

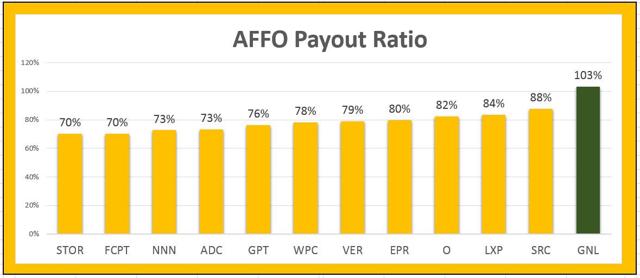

A majority of GNL’s assets are office buildings (59.5%) that require significantly more capital (capex) for tenant upfits, leasing commissions, and re-leasing costs. Recognizing that GNL’s average lease duration is around 9 years, however, most REITs with office exposure maintain lower AFFO payout ratios to provide an adequate margin of safety in the event of a tenant default.

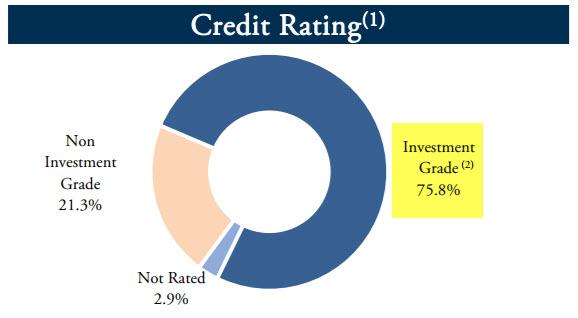

As I analyze the tenant roster, it"s apparent that there are many credit-rated tenants. The company states that 75.8% is leased to investment grade tenants.

However, there is a footnote in the Investment Presentation that reads:

“As used herein, “Investment Grade Rating” includes both actual investment grade ratings of the tenant or Implied Investment Grade. Implied Investment Grade includes ratings of tenant parent (regardless of whether or not the parent has guaranteed the tenant’s obligation under the lease) or lease guarantor. Implied Investment Grade ratings are determined using proprietary Moody’s analytical tool, which compares the risk metrics of the non-rated company to those of a company with an actual rating.”

So, if GNL seeks to differentiate itself as a credit buyer, it should also be competitive when it comes to its weighted average cost of capital (or WACC). After all, the REIT suggests that it is a consolidator of Net Lease buildings leased to "largely investment grade tenants", so it would seem reasonable to believe that it could be competitive as a buyer. Right?

What is GNL’s Competitive Advantage?

A few days ago, I wrote an article titled "Who Wouldn"t Want To Milk This Cash Cow?" In it, I explained:

“The most dominating “cash cows” will be these Net Lease REITs that are able to generate the most consistent and highest profits. While O and WPC are both exceptional REITs, based on their track record of dividend growth, there is only one Cash Cow King...”

I added:

“O can generate wider profit margins (investment spreads) while also reducing credit risk (by investing in higher quality investment grade properties).”

I provided a WACC illustration for Realty Income, and I explained that the REIT"s investment spreads relative to its weighted average cost of capital remained healthy and above the historical averages.

O: 3.16 AFFO estimate/$53 stock price = 6.0% Cost of Equity. Combined with 3.8% estimated cost of 10-year paper, WACC = 4.8%

Now let"s compare this to Global Net Lease (using apples to apples comparisons).

Here"s my back-of-the-napkin WACC score for GNL.

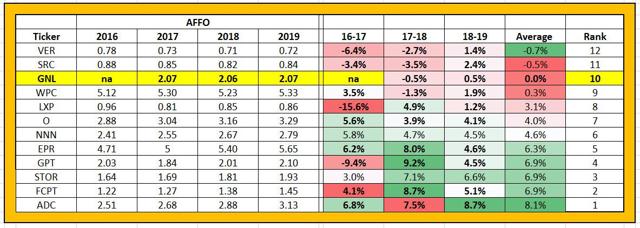

2018 expected AFFO/share: $2.06

Current stock price: $19.27

Cost of equity = $2.06/$19.27 = 10.7%

Cost of 10-year debt is tough because the REIT doesn"t have any 10-year unsecured outstanding, but let"s just assume something like 4.5% (that’s generous).

WACC (assuming 1/3rd debt) = 10.7% * .67 + 4.5% * .33 = 8.66%

To be clear, this is an "apple to apples" model, and to be fair, GNL uses much higher leverage (~50%) than this model. I used the 33% leverage because that is what a "normal Net Lease REIT" balance sheet should look like. Realty Income"s WACC is 4.8% - over 400 bps lower than GNL (on an apples to apples basis).

What does this mean?

With such a high cost of capital, it"s hard to believe that GNL can compete with peers such as Realty Income or W.P. Carey. It"s perplexing to see how GNL can grow AFFO/share by using 50% leverage, and clearly, the recent acquisitions are not accretive, based on the above-referenced WACC analysis.

How can GNL acquire properties "profitably" at 7.13% (above cap rate) when the WACC is 8.66%?

More Complexity

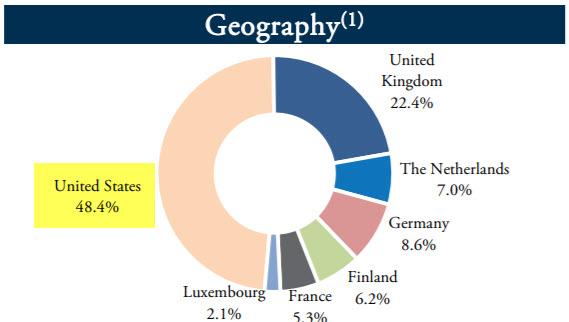

Not only is GNL"s balance sheet more levered than most Net Lease REIT peers, but the company also has significant complexity risk associated with its comprehensive hedging program. The REIT has just under 50% of its investments located outside of the United States.

Unlike W.P. Carey, an internally managed REIT, GNL is externally managed, and that means it technically it relies on Moor Park Capital to manage its European assets. This provides more complexity risk, and GNL is obligated to pay fees, which may be substantial, to its advisor and its affiliates.

It has no employees whatsoever, so as an investor in the company, you are paying out the following services:

- A base fee of $18.0 million per annum payable in cash monthly in advance ("Minimum Base Management Fee");

- Plus a variable fee, payable in cash monthly in advance, equal to 1.25% of the cumulative net proceeds realized by the Company from the issuance of any common equity, including any common equity issued in exchange for or conversion of preferred stock or exchangeable notes, as well as from any other issuances of common, preferred, or other forms of equity of the Company, including units of any operating partnership ("Variable Base Management Fee"); and

- An incentive fee ("Incentive Compensation"), 50% payable in cash and 50% payable in shares of the Company"s Common Stock (which shares are subject to certain lock-up restrictions), equal to: (A) 15% of the Company"s Core AFFO (as defined in the Advisory Agreement) per weighted average share outstanding for the applicable period ("Core AFFO Per Share")(1) in excess of an incentive hurdle based on an annualized Core AFFO Per Share of $0.78, plus (B) 10% of the Core AFFO Per Share in excess of an incentive hurdle of an annualized Core AFFO Per Share of $1.02. The $0.78 and $1.02 incentive hurdles are subject to annual increases of 1-3%. The Base Management Fee and the Incentive Compensation are each subject to an annual adjustment.

The annual aggregate amount of the Minimum Base Management Fee and Variable Base Management Fee (collectively, the "Base Management Fee") that may be paid under the Advisory Agreement are subject to varying caps based on assets under management ("AUM") (2), as defined in the Advisory Agreement.

In addition, the per annum aggregate amount of the Base Management Fee and the Incentive Compensation to be paid under the Advisory Agreement is capped at (A) 1.25% of the AUM for the previous year, if AUM is less than or equal to $5.0 billion; (B) 0.95%, if the AUM is equal to or exceeds $15.0 billion; or (C) a percentage equal to: (A) 1.25% less (B) (i) a fraction, (X) the numerator of which is the AUM for such specified period less $5.0 billion and (Y) the denominator of which is $10.0 billion multiplied by (ii) 0.30%, if AUM is greater than $5.0 billion but less than $15.0 billion. The Variable Base Management Fee is also subject to reduction if there is a sale or sales of one or more investments in a single or series of related transactions exceeding $200.0 million and, the special dividend(s) related thereto.

The Property Manager provides property management and leasing services for properties owned by the Company, for which the Company pays fees equal to: (i) with respect to standalone, single-tenant, Net Lease properties which are not part of a shopping center, 2.0% of gross revenues from the properties managed; and (ii) with respect to all other types of properties, 4.0% of gross revenues from the properties managed.

For services related to overseeing property management and leasing services provided by any person or entity that is not an affiliate of the Property Manager, the Company pays the Property Manager an oversight fee equal to 1.0% of gross revenues of the property managed.

Solely with respect to the Company"s investments in properties located in Europe, the Service Provider receives a portion of the fees payable to the Advisor equal to: (i) with respect to single-tenant, Net Lease properties which are not part of a shopping center, 1.75% of the gross revenues from such properties; and (ii) with respect to all other types of properties, 3.5% of the gross revenues from such properties. The Property Manager is paid 0.25% of the gross revenues from European single-tenant, Net Lease properties which are not part of a shopping center and 0.5% of the gross revenues from all other types of properties, reflecting a split of the oversight fee with the Service Provider.

Also, make sure you read the fine print:

The initial term of the Advisory Agreement expires on June 1, 2035...

Oh yes, I forgot that the management team referenced above is AR Global Investments.

One more risk, there’s a new CEO. Last July, GNL appointed Independent Director James Nelson to serve as its CEO and president starting August 15, 2017. Nelson will continue to serve on the company’s board of directors and replaced the Scott Bowman.

Before joining GNL, Nelson served as CEO with several public and private companies, including Orbitex Management, a $17 billion financial services company, and Eaglescliff Corp., a specialty investment banking, consulting and wealth management company, where he was also chairman from 1986 until 2009. Nelson served as a director of Icahn Enterprises LP (NYSE:IEP) and Voltari Corp. (NASDAQ:VLTC) from 2011 to 2015, and as chairman again, from 2012 to 2015.

Looks like a solid resume for a CEO, but I like IEP as much as I do GNL. Here’s what I said about IEP last year on Seeking Alpha:

“I believe that a stock with a strong history of earnings and dividend growth will ultimately outperform. I am not initiating a position in IEP. As a defensive investor, I must confine myself to shares of companies with a record of profitable operations and in strong financial condition.”

Nelson has only been CEO at GNL for less than a year, so I’m not going to be critical whatsoever. He has essentially inherited a “value trap”, and given the company’s cost of capital “disadvantage”, I believe it will perform like quick sand.

Remember that GNL has outsized office exposure, and this means there are considerably more costs to lease space, remodel space, and pay leasing fees (to brokers). There is essentially "no margin of safety" in terms of the company"s payout ratio. All it takes is one hiccup, and guess what...?

Also, this elevated payout ratio means GNL will have a difficult time growing its dividend. The company pays out $2.13/share in dividends, and the prospects for earnings growth are muted.

Net Lease REITs should be predictable, and based upon my analysis, GNL is riddled with complexity. More importantly, this REIT is a “sucker yield”, defined as follows:

“If a stock seems to pay a dividend yield that is exceptionally high, investors should look harder at the sources of payment behind the dividend. That is, how profitable is the company? Can the sources of income cover the dividend payment? How sustainable is the dividend? Are there threats to the underlying business model?”

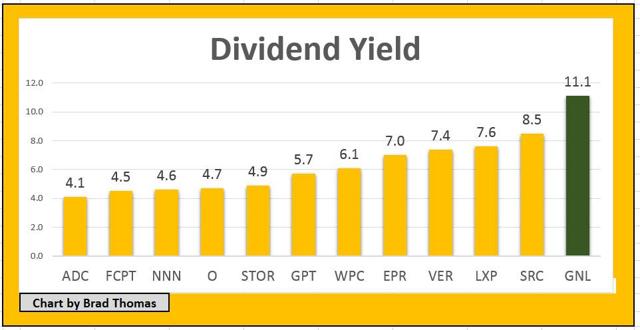

As far as I"m concerned, the market is pricing GNL squarely. There is plenty of cheese in the trap (11.1% dividend yield), and I don"t see any catalysts that suggest shares will move up "materially". Dane Bowler thinks the trap will spring, but until GNL provides a more predictable path for profits (i.e., lower cost of capital), I"m not convinced the shares will spring. Thus, this externally managed REIT is nothing more than a value trap!

Arguably, the fundamentals aren’t superior to the blue-chip REIT peers, as there is a reason my “cash cow king” deserves premium shelf space. There is very little incentive for GNL to outperform given that the external management team is raking fees under a long-term contract. In fact, based on the elevated payout ratio, investors are essentially risking all of their capital for the sake of the high dividend - or sucker yield.

“It’s important to recognize that there are two ways to make money in the stock market – capital appreciation and dividends. When a stock is paying an extraordinarily high dividend yield combined with an unsustainable business model, there will almost always be loss of principal.”

Investors should always proceed with caution and focus more on dividend safety than dividend yield. Be careful of chasing sucker yields, as the raised nail always gets hammered. Focus on quality, and don"t get too cute!

Note: Brad Thomas is a Wall Street writer and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos and be assured that he will do his best to correct any errors if they are overlooked.

Finally, this article is free and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking. If you have not followed him, please take five seconds and click his name above (top of the page).

Source: F.A.S.T. Graphs and GNL Investor Presentation.

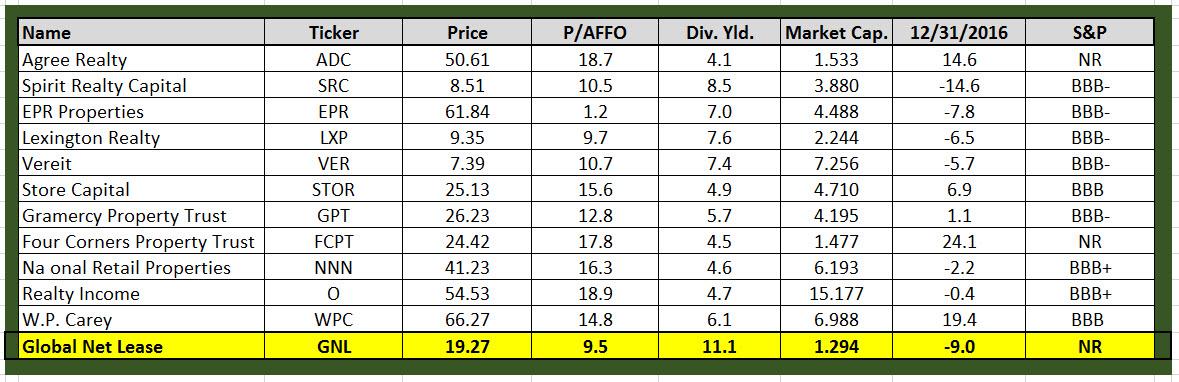

Other REITs mentioned: Agree Realty Corp. (NYSE:ADC), Spirit Realty Capital (NYSE:SRC), EPR, Lexington Realty Trust (NYSE:LXP), VEREIT, Inc. (NYSE:VER), STOR, Gramercy Property Trust (NYSE:GPT), Four Corners Property Trust (NYSE:FCPT), National Retail Properties (NYSE:NNN), O, and WPC.

PS: Thanks again, Dane. We don"t always agree, and I appreciate the value you bring to Seeking Alpha (and I"m sure many others do as well). I have no (long or short) position in GNL.

In a few days we plan to publish (exclusively for Marketplace subscribers) all of our property sector data weekly, including our recommendations and highly sought-after Rhino REIT Ratings.

REITs should be part of your daily diet and we would like to help you construct an Intelligent REIT portfolio, utilizing our portfolio modeling strategies.

The Intelligent REIT Investor is the #1 REIT Research site on Seeking Alpha. Brad Thomas and Rubicon Associates have a combined 40 years of investing experience. We publish exclusive research content on over 100 REITs, and our Durable Income Portfolio has returned over 12% YTD. We recently announced that the Small Cap REIT Portfolio has returned over 20% YTD.

Our service includes weekly property sector updates and weekly Buy/Sell picks. We provide most all research to marketplace subscribers and we also provide a “weekender” report and a “motivational Monday” report. We stream relevant real-time REIT news so that you can stay informed.

There is absolutely no reason to chase yield... let us do all of the heavy-lifting so you can "sleep well at night." Subscribe here

Disclosure: I am/we are long ACC, AHP, APTS, ARI, BRX, BXMT, CCI, CHCT, CIO, CLDT, CONE, CORR, CUBE, DDR, DEA, DLR, DOC, EPR, EXR, FPI, FRT, GEO, GMRE, GPT, HASI, HTA, IRET, IRM, JCAP, KIM, LADR, LAND, LMRK, LTC, MNR, NXRT, O, OFC, OHI, OUT, PEB, PEI, PK, QTS, REG, RHP, ROIC, SKT, SPG, STAG, STOR, STWD, TCO, UBA, UMH, UNIT, VER, VTR, WPC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment