Last month in "It"s A Mad, Mad, Mad World", I took a stab at explaining how and why cryptocurrencies represent a systemic risk.

Over the last year, I"ve developed a pretty solid understanding of Bitcoin, blockchain, and the cryptosphere in general. But if you"re a regular Heisenberg reader, you know that my definition of "solid understanding" is a bit different from most people"s definition.

Being able to talk intelligently about something isn"t even close to what I would consider sufficient when it comes to putting digital pen to digital paper. That"s why everything I"ve written about cryptocurrencies and Bitcoin over at Heisenberg Report revolves around price action, psychology, the reasons why cryptocurrencies aren"t viable as "money" and the possible knock-on effects for other assets and/or the broader economy (i.e. systemic risk).

I feel comfortable discussing those aspects of the cryptocurrency phenomenon because those discussions lean heavily on things I am extremely qualified to talk about. That is, when it comes to price action, investor psychology, what it means for something to be a currency (or to be "money", so to speak) and systemic risk, I have much more than a "solid understanding". In those matters, I"m a walking encyclopedia. What I do not posses encyclopedic knowledge of are the technological underpinnings of digital currencies. Again, I have a solid understanding of the technological points, but you"re not going to see me penning manifestos about why blockchain is or isn"t going to change the world or why Ripple can or can"t upend SWIFT.

Just to be clear, I don"t think developing that depth of understanding when it comes to the technology is important right now for anyone other than the people who are behind this movement and maybe a handful of academics who can perhaps help discern how the technology can actually be applied in a way that has some utility outside of speculation and/or outside of providing what Nassim Taleb has called "an insurance policy that will remind governments that the last object establishment could control, namely, the currency, is no longer their monopoly."

The reason I don"t think it"s necessary for the rest of us to get too bogged down in it is precisely because by the time it matters, something bad will have happened that will ultimately force governments to regulate cryptocurrencies so heavily that they will cease to be objects of public fascination and thus vehicles for speculation.

There are a number of things that can go wrong here, some of which obviously have to do with the potential for cryptocurrencies to serve ostensibly nefarious purposes, but what I try to zoom in on are the possible knock-on effects for traditional markets and also for the economy more generally.

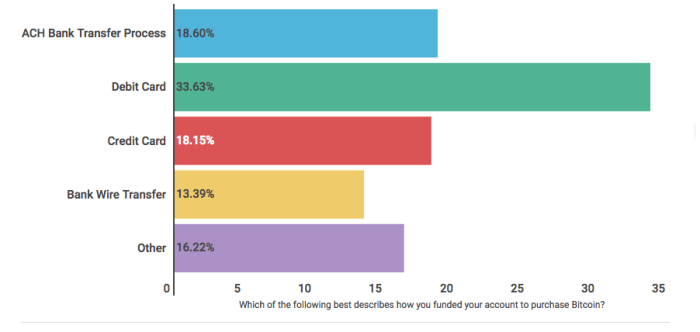

One particularly disconcerting development is that according to a LendEDU poll published the day after Bitcoin peaked in December, nearly 20% of people were using a credit card to get in on the craze:

(LendEDU)

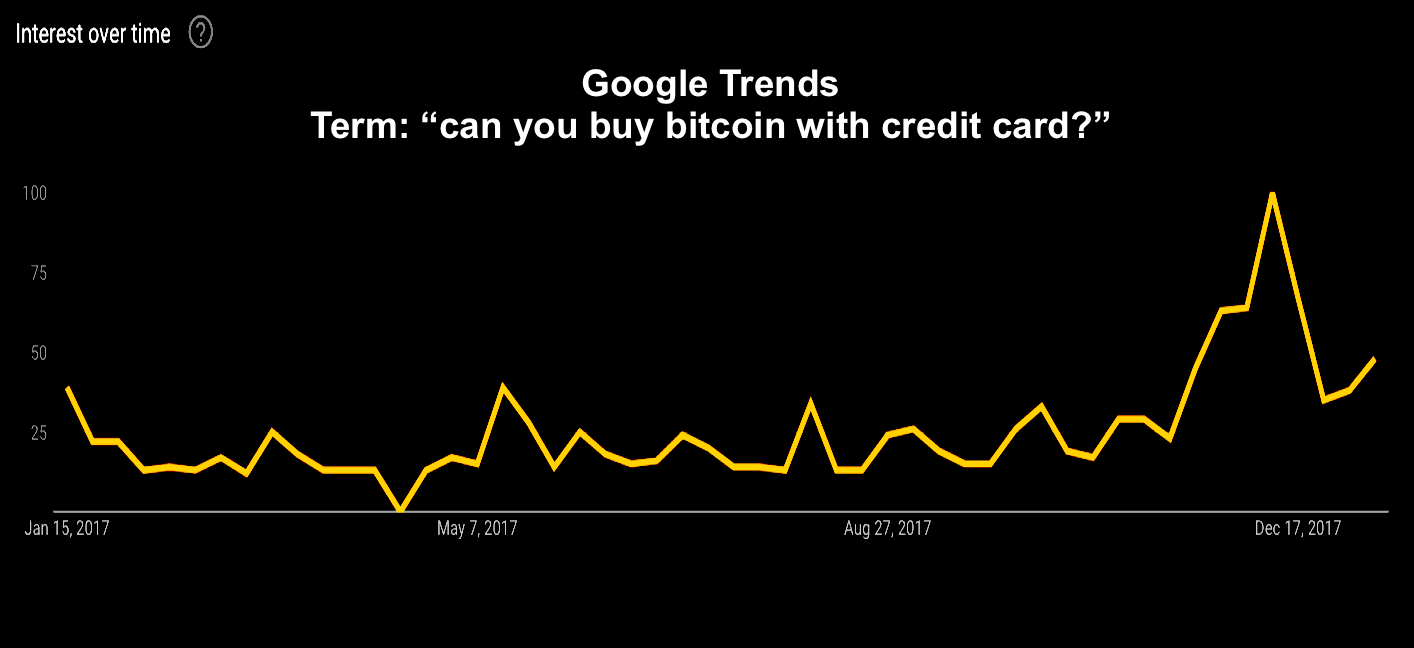

Hilariously (or not, depending on your penchant for dark humor), that actually coincided with a spike in Google searches for "can you buy Bitcoin with a credit card?":

(Google Trends)

Correlation doesn"t equal causation, but it seems like some coincidence that the publication of the poll cited above, the peak in that Google Trends chart, and Bitcoin"s high at roughly $20,000 all came within the same 48-hour window.

The risk there is clear. That effectively represents a high interest loan collateralized by an "asset" that"s depreciated by roughly 50% over the ensuing month. The chances that ends up showing up in, for instance, banks" losses on credit cards are probably low, but you can"t rule it out.

On top of that, at least one bank recently "went there" by trying to estimate what the "wealth effect" (i.e. an increase in consumers" propensity to spend based on unrealized gains in financial assets) might be from Bitcoin trading in Japan. The fact that anyone is even talking about that is unnerving. If, for instance, consumers did in fact end up spending more based on gains in their cryptocurrency accounts and that was reflected in high level economic data, the sugar high from that could evaporate in the event those unrealized crypto gains disappear. That could create noise in the data and make q/q and m/m compares more difficult, complicating policymaker reaction functions.

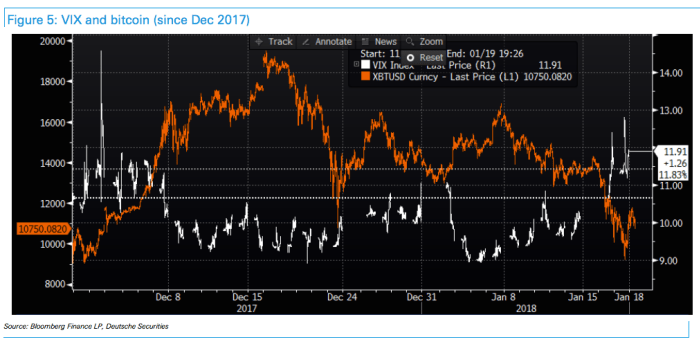

But beyond all of that, it"s becoming increasingly likely that traditional risk assets will begin to take their cues from the crypto market. Deutsche Bank was out with a great note this week describing how, far from the "safe haven" status crypto proponents often ascribe to Bitcoin, cryptocurrencies in fact represent exactly the opposite. That is, they represent the new frontier in risk-taking, replacing short vol. as the proxy for risk sentiment. Here"s the bank"s Masao Muraki:

The current ‘triple-low environment’ of low interest rates, low spreads, and low volatility has given birth to new asset classes like implied volatility (ETFs selling volatility), and cryptocurrencies. The prices of both asset classes have plummeted and rebounded simultaneously and in 2018, correlation between Bitcoin and VIX has increased dramatically.

The problem here is that just as the proliferation of strategies that explicitly or implicitly rely on the low-volatility environment continuing has the potential to create a "tail wagging the dog" dynamic whereby vol. spikes force selling in the underlying, if cryptocurrencies are increasingly viewed by larger investors as a proxy for risk sentiment, sharp moves have the potential to spill over. Here"s Deutsche again:

Cryptocurrencies are closely watched by retail investors, affecting their risk preferences for stocks and other risk assets. Although institutional investors recognize that stocks and other asset valuations may have entered bubble territory (US equities’ average P/E is around 20x), they cannot help but continue their risk-taking. Now, a growing number of institutional investors are watching cryptocurrencies as the frontier of risk-taking to evaluate the sustainability of asset prices. The result is that institutional investors, who are supposed to value assets using their sophisticated financial literacy, analysis, and information-gathering strengths, are actually seeking feedback about the market from cryptocurrency prices (which are mainly formed by retail investors). We believe the correlation between Bitcoin and VIX can increase as more institutional investors begin trading Bitcoin futures.

Underscoring that is a new piece out in the Wall Street Journal that documents the extent to which retail brokerages are seeing an avalanche of inflows from what they say are first-time investors (millennials are specifically named) attempting to capitalize off the gains in crypto-related stocks and, when they"re allowed to trade them, Bitcoin futures. Here"s the Journal:

Discount brokerages TD Ameritrade Holdings Corp., E*Trade Financial Corp. and Charles Schwab Corp. reported surges in client activity at the end of 2017 that have accelerated in January. The firms attributed much of the activity to retail, or individual, investors who are opening brokerage accounts for the first time, some of them lured by the boom in cryptocurrency and cannabis investments.

[...]

“Crypto and cannabis…volumes have been up big,” E*Trade Chief Executive Karl Roessner said Friday on the firm’s fourth-quarter earnings call with analysts and investors. Despite the bitcoin-futures offering not being “a material offering,” Mr. Roessner said about a 10th of daily average revenue trades—a key metric for brokerages—has so far this month been blockchain- or pot-related.

Keep in mind that the obvious risks in inherent in all of that come on top of the risk associated with clearing crypto derivatives with other assets. Those risks were laid out in an open letter to the CFTC penned by Thomas Peterffy, the billionaire founder and chairman of Interactive Brokers, back in November.

Earlier this month, the Cboe"s suggested that futures on other cryptocurrencies could eventually be in the cards. To wit, from comments Chris Concannon, Cboe’s president and chief operating officer, made at a press briefing in New York:

You look at the entire crypto space and you look at what other products have the liquidity and the notional size, a derivative makes sense.

I guess that depends on your definition of "makes sense". For now, crypto ETFs are still getting quite a bit of pushback from the SEC, but it"s probably just a matter of time before we cross that bridge as well.

But irrespective of how this develops, crypto risk is already embedded in markets and to a lesser extent in the broader economy as detailed above. And I could give you a long list of other arguments to support the same contention.

To be clear, more and more people are starting to voice concerns about spillover effects. For instance, Wells Fargo"s Chris Harvey has been very vocal about the risk to stocks over the past couple of months. Here"s what he told CNBC in his latest appearance on the network:

We see a lot of froth in that market. If and when it comes out, it will spill over to equities. I don"t think people are really ready for that.

No, people are probably not "ready for that". And part of the reason no one is ready is because it"s not clear that everyone understands the points Deutsche Bank made in the note cited and excerpted above.

What all of this suggests for investors is that you"re going to have to start watching cryptocurrencies the same way you might watch the VIX. If it"s true that larger investors are going to start using cryptocurrencies as a proxy for risk sentiment, well then you might want to start asking yourself what that might mean in terms of the potential for a large drawdown in the space to impact what you previously assumed were unrelated assets.

I"m not saying you should obsess over every tick in Ripple, but when you see things like that $400 million theft from Coincheck on Friday, you should consider that fair warning about how unstable that market really is.

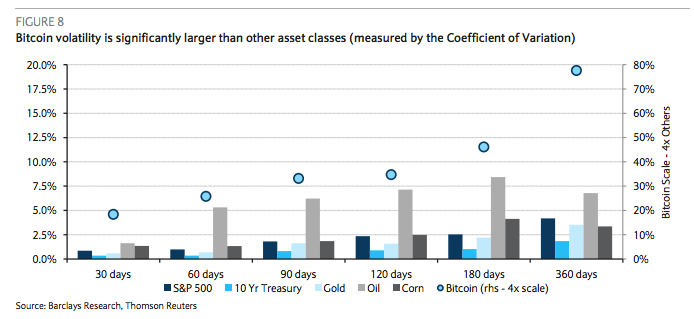

One last thing: I"m not sure the flipside of everything said above is ever going to be true. That is, even if Bitcoin and other cryptocurrencies have another year like 2017, you"re never going to be able to reliably extrapolate anything from that about a positive wealth effect for the economy or for increased risk appetite in equities. Why? Simple: because cryptocurrencies are so volatile that any of the positive externalities from a sharp rally have to be discounted because they can all be negated virtually overnight. You cannot extrapolate anything on the positive side from appreciation in an asset that, like Bitcoin, is 15-25x as volatile as the S&P, 20x-40x as volatile as gold, and 5x-11x as volatile as oil (according to Barclays and as measured by the coefficient of variation):

(Barclays)

Nothing further. For now.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor"s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

No comments:

Post a Comment