In Is Altria A Cigar Butt? I concluded:

The recent significant price drop in Altria"s shares have made it, in my opinion, a better "hold" than its competitors, primarily because governments across the world will likely follow in the FDA"s footsteps towards tighter regulation of nicotine levels.

If you must own shares in a cigarette company, because of its steady top-line growth and improving profit margins as well as lower balance sheet leverage, Altria is a better option as compared with its competitors.

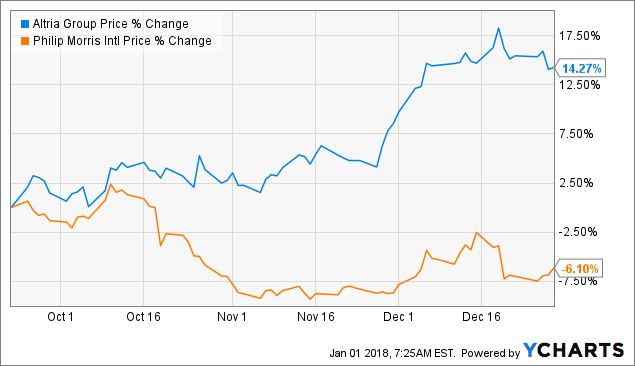

The following is how Altria (MO) has performed against a comparable company Philip Morris (PM) since the article"s publication:

MO data by YCharts

In less than three months Altria has outperformed Philip Morris by more than 20%. This alone would make a portfolio manager"s year.

As I discussed in Why Did Philip Morris Really Sink?, Philip Morris has severe problems, which can only worsen if what Reuters recently described in an investigative piece on the company"s IQOS product is true:

Former employees and contractors have detailed irregularities in the clinical experiments that underpin Philip Morris International"s application to the FDA for approval of its iQOS smoking device. The agency is expected to decide by next year on whether the tobacco giant can sell its new product in the U.S.

IQOS, which allows the smokers to heat the tobacco instead of burning it, and which, according to Philip Morris, avoids subjecting smokers to the same levels of carcinogens and other toxic substances found in a regular cigarette is also important to Altria, Philip Morris" former parent company, because:

If the FDA approves the application, that would raise the possibility of Philip Morris International"s former parent company and U.S. partner, Altria Group Inc, capturing market share in a nation where overall cigarette sales plummeted more than 30 percent between 2005 and 2016.

In other words, the product that is supposed to replace the revenues, and most importantly, the extreme profit margin of traditional cigarettes is now under heavy scrutiny following severe accusations by former employees. This is significant.

Implications For Investors

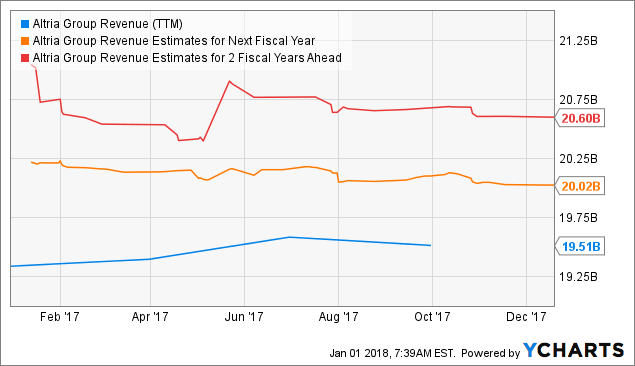

Altria"s revenues are projected to increase for the next two years:

MO Revenue (TTM) data by YCharts

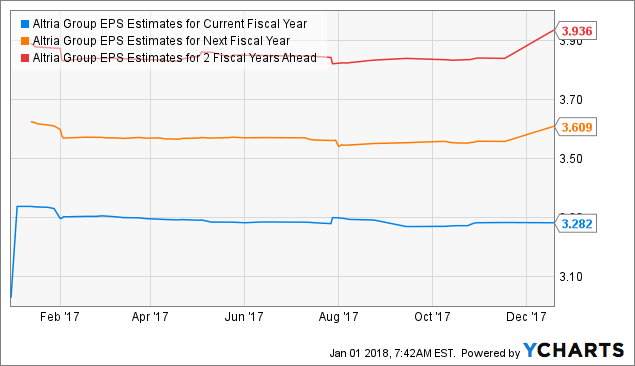

The company"s earnings are also set to grow meaningfully in the same period:

MO EPS Estimates for Current Fiscal Year data by YCharts

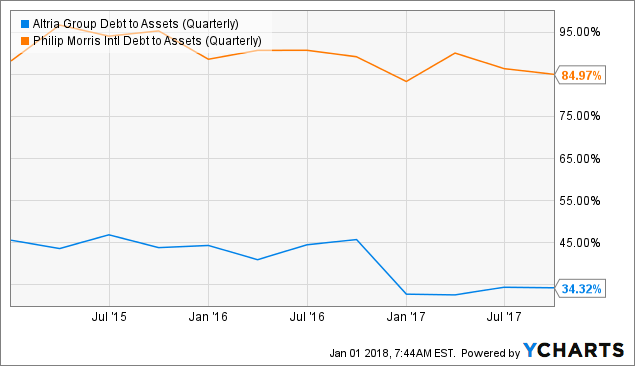

On the risk side, Altria"s debt to asset ratio remains at a significantly more manageable level compared to that of Philip Morris:

MO Debt to Assets (Quarterly) data by YCharts

In other words, Altria"s growing revenues and earnings, combined with its low debt-to-asset ratio, still makes it the clear preferred play among the two options, for now.

Risks Are Mounting

On July 28, the shares of cigarette companies dropped significantly across the board when the U.S. Food and Drug Administration ("FDA") announced that it plans to reduce nicotine levels to a point where it is not addictive:

The overwhelming amount of death and disease attributable to tobacco is caused by addiction to cigarettes - the only legal consumer product that, when used as intended, will kill half of all long-term users.

Addiction to cigarettes is arguably the key to cigarette companies" high profit margins: customers are willing to pay higher and higher prices in order to satisfy what they see as a fundamental need. The FDA"s decision to reduce nicotine levels and fight addiction is, in a way, a fight against extreme profit margins made possible by addiction.

In addition, the product that is allegedly safer and supposed to replace the extreme margins of traditional cigarettes is under heavy scrutiny and may never be brought to market in the United States. For me, the Reuters investigative piece greatly increases the discount rate that should be applied to management claims around future revenues and profits assigned to IQOS.

Bottom Line

Altria remains the preferred option among cigarette companies, if and only if, one must own shares in a cigarette company. Given the mounting risks, however, it may be wise to consider selling the stock now that the year-end is behind us, which may be significant for some investors for tax purposes.

All in all, I see better opportunities elsewhere.

Follow For Free Articles

If you enjoyed this article, please scroll up to the top of the page and click the "Follow" button next to my name. Your support will allow me to invest further time and resources into creating proprietary research for you.

Premium Research

If you"re interested in learning about my investment methodology as well as high-quality fundamental research on Tesla, supported by detailed financial projections by product and service line, including years 2019 and beyond, as well as timely price target alerts and weekly Live Chat community discussions, join Tesla Forum. I"m confident that you will find my research to be very insightful, and I look forward to discussing ideas with you.

Disclosure: I am/we are long TSLA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment