Yesterday, rumors began swirling that General Electric (GE) might be of interest as a significant investment, or even as a takeover candidate, from none other than Warren Buffett"s Berkshire Hathaway (BRK.A) (BRK.B). So enthusiastic were investors that GE might finally catch a break that shares went up as much as 6.5% - no small sum that represents over half a billion in market capitalization.

Unfortunately, dreamers that bought GE are likely to be disappointed. Here"s why.

Buffett"s past with GE

Ten years ago, the Oracle of Omaha famously invested $ 3 billion in GE preferred stock at the height (or perhaps in the depths?) of the Great Recession. The preferred shares, superior in dividend preference to common stock but inferior to debt, came at a high price for "The General": 10% interest per year in perpetuity. If GE wanted out, it could repurchase Buffett"s preferred stock at a 10% premium (which it did for a total of $ 4.1 billion, including dividends, in late 2011). As icing on the cake, Buffett"s Berkshire received warrants to purchase nearly 135,000 shares of GE"s stock at $ 22.25 per share.

If this sounds like a sweet deal for Buffett, you"re right - it borders on usurious. It"s good to be The Oracle, after all.

A struggling giant

Now, a decade later, GE is faced with a different problem. Macroeconomic storms have given away to microeconomic travails:

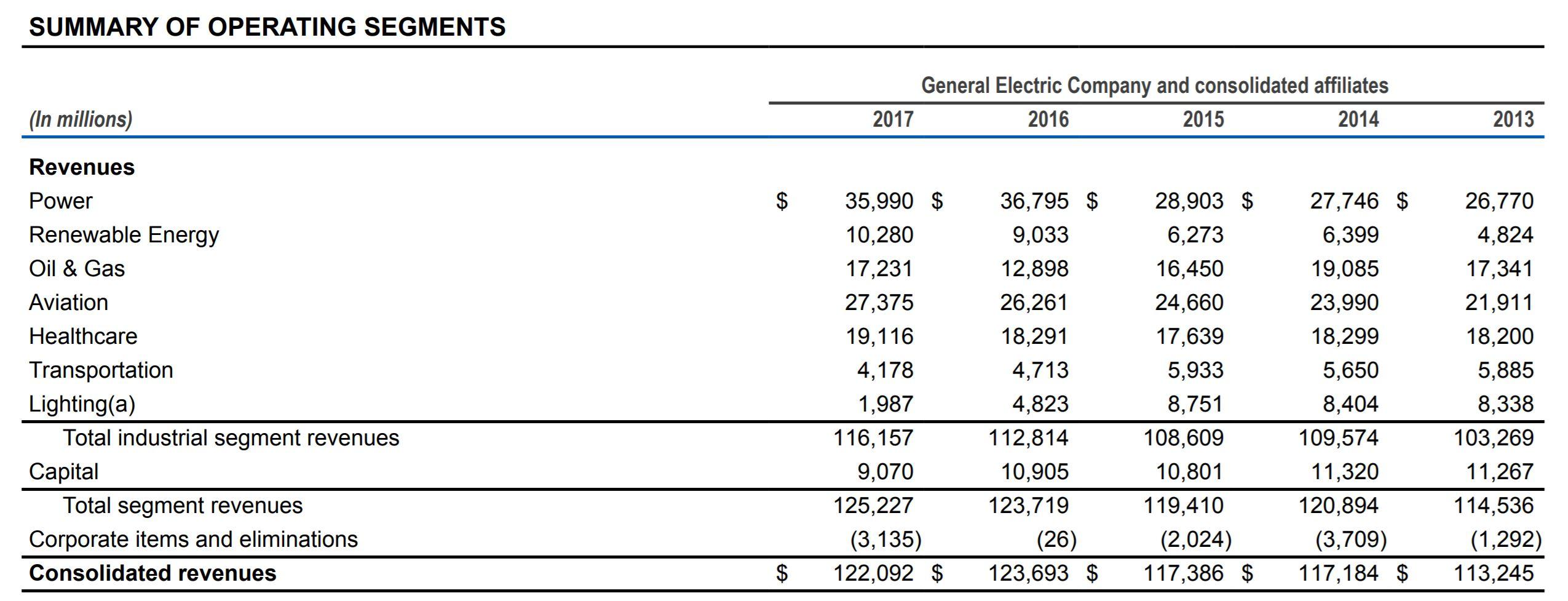

General Electric Selected Financial Results

| FY 2015 | FY 2016 | ||

| Total Revenue | $ 117.4 billion | $ 123.7 billion | $ 122.09 billion |

| Gross Profit | $ 32.09 billion | $ 33.4 billion | $ 17.99 billion |

| SGA Expenses | $ 21.9 billion | $ 19.36 billion | $ 20.44 billion |

| Operating Income ( Loss) | $ 11.65 billion | $ 14.05 billion | ($ 3.9 billion) |

| Net Income | ($ 6.12 billion) | $ 8.83 billion | (5.8 billion) |

| Free Cash Flow | $ 12.58 billion | (7.44 billion) | $ 3 billion |

Data Sources: General Electric, Scout Finance.

The winding down of GE Capital, as well as other "one-time items" has distorted GE"s net income. But, as Buffett"s teacher Benjamin Graham pointed out in The Intelligent Investor, why ignore such costs in valuing a business? Graham knew that a company of any reasonable size (and especially enterprises of GE"s scale) will ALWAYS have expenses like this crop up.

The more reliable figure for a quick-and-dirty analysis, free cash flow, is flashing an alarm bell (Fun fact: GE"s free cash flow, according to our friends at Scout Finance, came in at a whopping $ 15.12 billion in 2013 and a staggering $ 20.6 billion in FY 2014.) What a difference a few years makes.

Buffett knows this, and he will inevitably look to each division"s results for signs that the ship can be righted. Unfortunately, the prognosis here is not good:

Source: General Electric FY 2017 10-K. Source: General Electric FY 2017 10-K. By shedding GE Capital, "The General" was getting back to its industrial roots. Unfortunately, its industrial roots aren"t exactly growth businesses these days (save for Renewable Energy, but even that represents a small portion of the whole). Any buyout of GE means you get the whole thing - and the whole is not thriving. John Flannery now leads the company, acknowledged to be a smart company man and touted as the man who turned around GE Healthcare. Alas, Healthcare"s performance over the past three years, the approximate period Flannery was at the helm, was not anything to write home about (see above). Flannery seems to have the situation in hand (which unfortunately forced him to cut GE"s dividend and plan large cost cuts). The problem is that the situation is an extremely tough one and almost certainly not something Buffett would want to dive into. That is unless GE is willing to part with one of its top performing divisions, of course. Arguably, Buffett made his first millions as a distressed investor and turnaround artist. Anyone who has read just one of the numerous biographies of the man has no doubt heard the tale of Dempster Mill Manufacturing, GEICO, and even a New England textile manufacturer named Berkshire Hathaway. But those days are over. Buffett wants to buy great businesses at fair prices - low stress is the name of the game. Not only that but Buffett"s other well-known "opportune" investments in national brands (made at a time of distress) all had one of two characteristics: (1) The source of trouble is immediately solved with capital. The simple need for cash was the case with Buffett"s 1970s investment in GEICO when the company needed cash to survive, but the fundamental business of providing low-cost insurance to government employees remained intact. Once the capital infusion occurred, the insurance regulators backed off. Or (2), the business itself is excellent, but the company has a dark cloud over it. This was the case with Buffett"s investment in American Express (AXP) in the 1960s. General Electric is different. A pile of money won"t solve its woes (although that wouldn"t hurt given the company"s debt load) and most of its businesses are barely growing - if that. So, no, Buffett won"t be buying a massive stake in GE nor will be gobbling up the whole thing. Buffett will not be riding in to rescue GE on a white horse. Could I be wrong? Absolutely. Buffett has unmatched insights and access to information (how often do you suppose he and Flannery have talked in the past few months?). Combining any one of GE"s businesses with Berkshire"s could lead to significant cost savings - a potential source of upside that few possess. Or perhaps he could call up his friends over at 3G Capital for some good old fashioned zero-based budgeting magic. But I doubt it. It SOUNDS like the cap to a fantastic investing career. But it wouldn"t be Buffett. If anything, he"s talking to Flannery at the time of this writing about acquiring one of GE"s better performing industrial businesses. I can only hope Mr. Flannery takes a pass. The worst thing one can do in a crisis is make a deal on onerous terms, a lesson I can only hope GE learned in its previous dealings with Mr. Buffett. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Buffett"s Cash Won"t Fix GE

What you need to know

Tech

No comments:

Post a Comment