(Source: imgflip)

The goal of my dividend growth retirement portfolio is to achieve market-beating double-digit total returns over time by building a well-diversified collection of top-grade companies bought at fair value or better. This means that I"m often willing to be "greedy when others are fearful" and buy stocks in badly beaten-down sectors and industries.

Well, few industries have been as brutalized in recent years as the midstream space, which has faced a perfect storm of negative factors, including:

- the worst oil crash in over 50 years (crude plunged 76% peak to trough)

- interest rates rising off all-time lows

- a market correction + trade-related volatility

- a tax rule change from the Federal Energy Regulatory Commission or FERC

All told, these factors have caused MLPs and midstream companies to fall into a bear market from which they have not yet recovered.

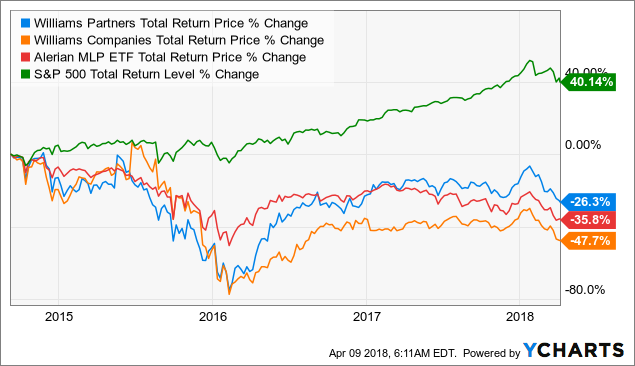

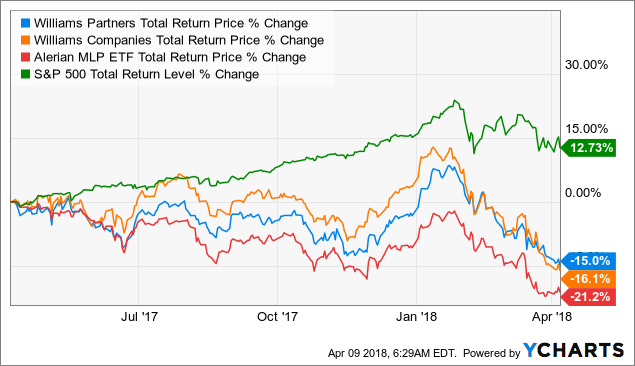

WPZ Total Return Price data by YCharts

Williams Partners (WPZ) and Williams Companies (WMB) are some of the largest names in this unloved industry, and both have seen more than their fair share of troubles in recent years. That includes a fiasco of an attempted merger between Williams and Energy Transfer Equity (ETE), as well as a failed buyout of Williams Partners by its sponsor.

The result has been large payout cuts for investors in both stocks. Meanwhile, Williams has embarked on an ambitious turnaround plan that management claims will result in generous, safe, and fast-growing distributions/dividends for years to come.

Readers have been requesting I take a look at this fallen midstream giant, so let"s take a look at how Williams" growth prospects are faring. Also, discover the pros and cons each stock offers investors. But most important of all, learn why I still can"t recommend either in the face of superior and lower risk blue chip rivals trading at even more appealing valuations.

Williams Partners: Fallen Pipeline Giant Is Turning Things Around

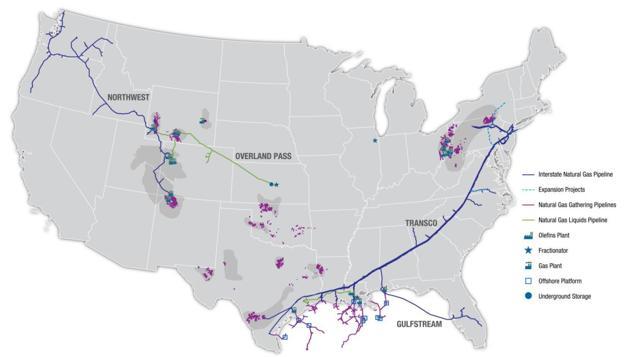

Originally founded in 1908 (went public in 2005), Williams Partners is an MLP that"s 74% owned by Williams Companies, its sponsor and general partner. Williams owns one of America"s largest natural gas pipeline systems consisting of 33,000 miles of pipelines that helps to move 30% of all US natural gas.

(Source: Williams Companies)

Its crown jewels are its:

- Transco pipeline

- Gulfstream pipeline

- Northwest pipeline

The Transco pipeline is a 9,700-mile 13-state system with 15 billion cubic feet per day in capacity that connects the Marcellus and Utica shale formations (Williams gathers 33% of this gas production), with two key growth markets. The first in America"s fast-growing liquefied natural gas or LNG industry, and the other is large northeast cities like New York City, Boston, and Philadelphia. Despite their close proximity to cheap shale gas formations, northeast cities pay some of the highest gas prices in the country.

Meanwhile, Williams" 50% ownership of Gulfstream (Spectra Energy (NYSE:SEP) owns the other half), provides the State of Florida with 60% of its gas supply. In fact, 75% of Florida"s natural gas-fired power plants are serviced by Gulfstream, whose average remaining contracts are 12 years long.

Finally, the Northwest pipeline is a 3,900-mile bi-directional pipeline with a capacity of 3.8 billion cubic feet per day that connects 11 states. This pipeline provides 90% of Washington State"s gas. The bi-directional system provides access to the Rocky Mountain and San Juan Basin gas supplies.

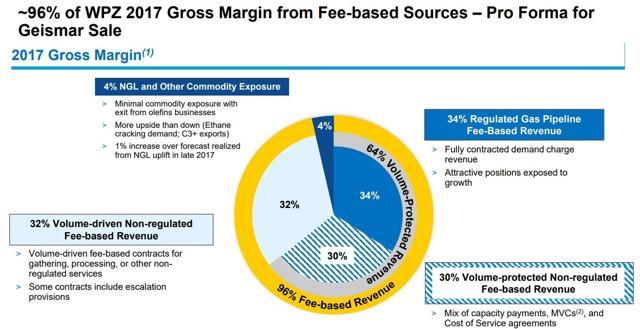

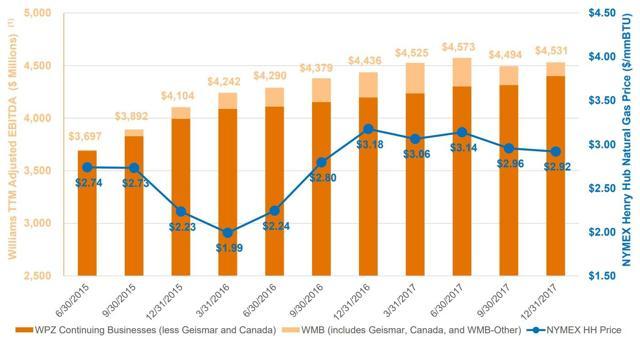

The key to Williams" investment thesis is the highly stable nature of its cash flows, courtesy of 96% of its revenue being under fixed-fee contracts, 64% of which are volume-protected. In other words, Williams" cash flow has almost no commodity exposure which is what allowed its adjusted EBITDA to hold up so well despite gas prices collapsing in 2015 and early 2016. Williams" interstate pipeline contracts are for between 15 and 20 years in duration, and its gas-gathering contracts are for 10 to 20 years when new.

(Source: Williams Investor Presentation)

However, if Williams" assets are so wide moat, and with such a stable source of cash flow, then what went wrong and forced those painful payout cuts? Well, several factors.

For one thing, Williams Companies and Energy Transfer Equity embarked on a remarkably ill-timed $38 billion deal in which ETE would acquire WMB and thus replace it as Williams Partners" sponsor. Due to the oil crash and drastically falling unit prices, that deal ultimately fell apart.

While management was being distracted by the highly complex ETE merger, the near-collapse of the US shale industry caused credit and equity markets to freeze out MLPs. That was due to fears that bankrupt producers would default on those long-term volume committed contracts.

This was especially hard for highly leveraged MLPs like Williams Partners which had spent the boom years retaining essentially no distributable cash flow (MLP equivalent of free cash flow and what funds the distribution). Instead, WPZ funded its growth through debt and equity issuances.

(Source: Williams Investor Presentation)

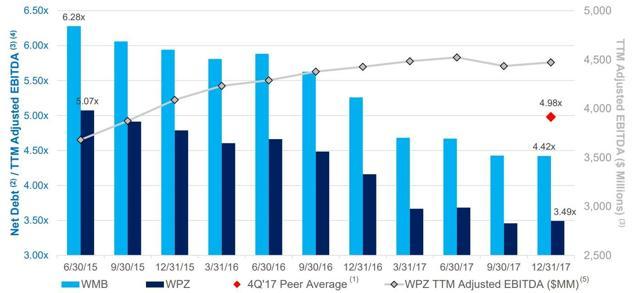

That worked fine as long as record low interest rates meant that MLPs had access to both very cheap equity and debt. However, the oil crash ended that and Williams found its leverage ratio (debt/Adjusted EBITDA), of 6.3 was putting its investment-grade credit rating at risk.

And with the unit price in the toilet, its cost of equity was rising too high, especially considering its incentive distribution rights were sucking 50% of marginal DCF away to its sponsor.

So, Williams had to make some very hard choices to adapt to these challenging industry conditions. Williams Partners announced the buyout of WMB"s general partner stake and incentive distribution rights which were threatening its ability to grow profitably.

The $11.4 billion deal, in which WPZ bought outs its sponsor"s IDRs for 289 million new units (WMB now owns 74% of WPZ), resulted in a painful but necessary 29% distribution cut. However, it also means that going forward, Williams Partners will be able to grow more profitably and hopefully sustain a safer and faster-growing payout.

The other major turnaround effort included selling over $3.3 billion in assets, specifically those that had high commodity exposure which created more volatile cash flow. That meant nearly all of the natural gas liquids or NGL businesses, as well as its Canadian assets.

Well, Williams has now completed both parts of this turnaround, and the results, while not pretty, mean it"s a far stronger income investment going forward.

Metric | 2017 Results | |||

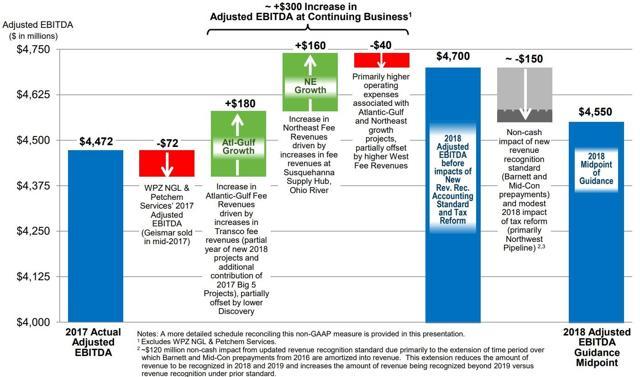

Adjusted EBITDA Growth | 1% | |||

Distributable Cash Flow Growth | -5% | |||

Distribution/Unit | -29.4% | |||

Distribution Coverage Ratio | 1.23 |

Metric | Guidance | |||

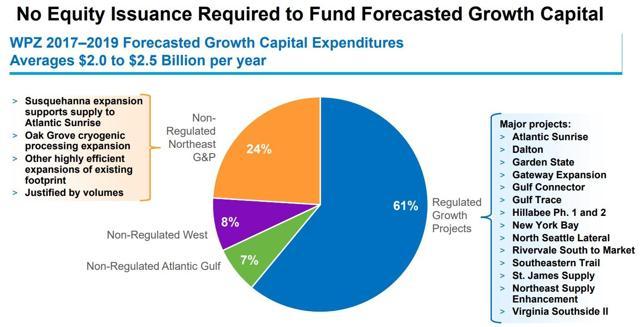

Growth Capex | $2.7 billion | |||

Adjusted EBITDA | $4.55 billion (+2%) | |||

DCF | $3.05 billion (+8%) | |||

Distribution Coverage | 1.24 | |||

Distribution Growth (2018 and 2019) | 5% to 7% |

Approximate Cash Cost Of Capital | 6.0% | |||

Historical DCF Yield On Invested Capital | 7.3% | |||

Gross Investment Spread | 1.3% |

Metric | 2017 Results | |||

Adjusted EBITDA | 2.1% | |||

DCF | -20.7% | |||

Dividend/Share | -28.6% | |||

Dividend Coverage Ratio | 1.46 |

Metric | 2018 Guidance | |||

Dividend Coverage | 1.35 | |||

Dividend Growth (2018 and 2019) | 10% to 15% |

Approximate Cash Cost Of Capital | 4.2% | |||

Historical DCF Yield On Invested Capital | 4.7% | |||

Gross Investment Spread | 0.5% |

Stock | Yield | Payout Coverage | Projected 10 Year | Potential 10 Year Annual Total Return |

Williams Partners | 7.2% | 1.23 | 4% to 8% | 11.2% to 15.2% |

Williams Companies | 5.6% | 1.46 | 9% to 13% | 14.6% to 18.6% |

S&P 500 | 1.9% | 3.3 | 6.2% | 8.1% |

Stock | Total Debt/Adjusted EBITDA | Interest Coverage | Credit Rating | Avg Interest Rate |

Williams Partners | 3.7 | 5.4 | BBB | 5.00% |

Williams Companies | 4.6 | 4.2 | BB+ | 5.20% |

Industry Average | 4.4 | 4.5 | NA | NA |

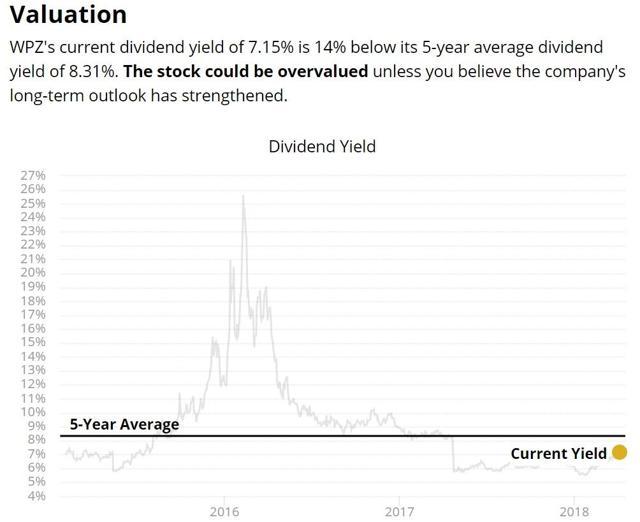

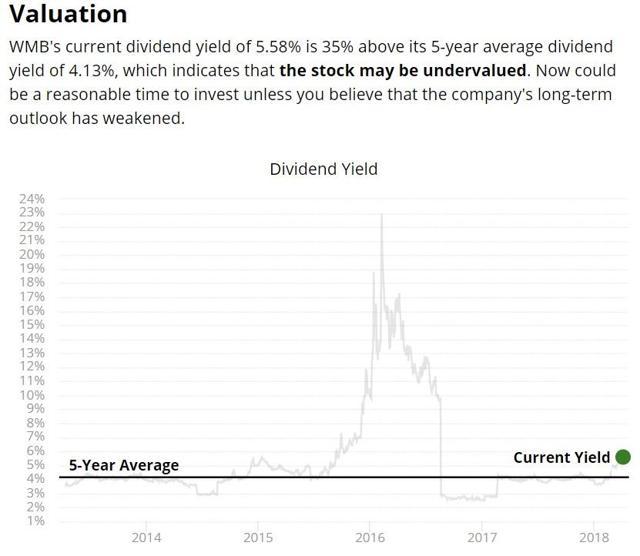

Stock | P/DCF | Yield | Historical Yield | Percentage Of Time Yield Has Been Higher |

Williams Partners | 11.3 | 7.20% | 5.00% | 18% |

Williams Companies | 13.9 | 5.60% | 3.40% | 5% |

{kind=link}

No comments:

Post a Comment